If you’re a sole proprietor who’s been in business for a while, you may wonder if and when you should incorporate yourself.

Recognizing the benefits that necessitate incorporation is crucial for determining when to adjust your legal structure.

After all, your business structure can make a big difference in your bottom line.

Should I incorporate?

As a sole proprietor, you’re personally liable for any debt or lawsuits incurred by your business.

When you incorporate, you’re not just creating a separate business entity. You’re also taking a significant step towards reducing your liability. This is a substantial benefit that provides a sense of security and protection that you can’t ignore.

This means you can protect personal assets like your home and other valuables from being at risk.

When you wonder if you can personally pay back any debt from your company, begin hiring employees, and worry about being able to manage any lawsuits from employees or customers personally, then consider incorporating your business.

Other reasons to consider incorporating are if there are multiple founders, if you want to raise capital, or if you want a clear exit strategy for your business.

All of these would be good reasons to form a corporation.

Always seek professional advice when making significant decisions about your business structure. This will provide you with support and guidance, knowing you’re making the right decisions for your business.

How do I choose a business entity?

It’s good to know the different legal entity options and be able to choose the one that’s right for you. This gives you control over your business structure and operations and makes you feel more confident in your decisions.

1. Sole proprietorship

A sole proprietorship is the simplest and easiest business structure to set up and run. Register your sole proprietorship as a ‘doing business as’ (DBA) name. This is a good option for small businesses with no assets.

2. Partnership

A partnership is when two or more individuals go into business together. Partnerships can have different levels of personal liability protection.

With a partnership, the profits and losses are reported on each individual’s tax returns through pass-through taxation. This is called a pass-through entity.

3. Limited liability company

A limited liability company or (LLC) also has limited liability protection. An LLC is in between a partnership and a corporation.

4. Corporations

Corporate structure divides corporations into two categories: C or S corporations. S corporation election protects personal liability and is a pass-through entity for your individual tax return.

C corps have the most personal liability protection, but their taxes are much higher because corporate profits are double-taxed at the personal and business levels.

How do I incorporate my business?

Here’s a simplified incorporation process breakdown if you're considering incorporating. This should help you understand the process and make it seem less overwhelming.

1. Create a business entity.

First, you’ll want to start the business formation process by:

Choose the state you’ll incorporate in. This can be your home state, but you must have an active office in the state in which you choose to file your business.

Choose a business name. It must be different from an already registered business.

Generate and file the Articles of Incorporation in the state in which your business is based. The Department of Commerce or Secretary of State usually files and issues the Articles of Incorporation, which include information such as the location, purpose of the company, and stock shares.

Pay the fee, which varies by state.

The state will process your filing and issue you a Certificate of Incorporation.

Designate a president, treasurer, officer, director, chief financial officer, and shareholder. You can fill these roles or hire someone to do it for you.

Appoint a registered agent to receive legal documents on behalf of the company. The registered agent must have a physical address in the state where the business is registered. While we’re on the topic of registered agents, be on the lookout for Shoeboxed’s upcoming registered agent service!

Hold a first directors’ meeting.

Write by-laws to define the roles of the officers, directors, and shareholders.

Issue stock certificates to anyone who’s an owner of the corporation.

The process may vary by state, so check with the secretary of state in the state you plan to incorporate to ensure you’re meeting all requirements.

2. Get a tax ID # from the IRS.

Once the business entity is created, you must get an employer identification number (EIN) from the IRS’s website.

This is done using IRS form SS4.

3. S Corp election.

If you choose S corporation status, you must complete IRS Form 2553 and file it with the IRS.

This must be filed within 2 1/2 months of your entity’s creation.

4. State tax IDs.

You’ll also need a state tax identification number or employer account number from the state.

These must be given to your payroll service.

You’ll also need a sales tax ID to sell retail products.

5. State and city licenses.

You may need to apply for a business license with the state.

You must register for a business license with the city and pay the city’s business tax.

What are the best practices to follow?

Once all the legal requirements are met, there are some best practices in corporate governance to follow to make your corporation run more smoothly and efficiently.

1. Keep your business finances separate from your personal finances by opening a business bank account.

You can open a business bank account once you have your federal tax ID number.

You should also apply for a business credit card.

Both will make tax time much easier since they separate business activities from personal transactions.

2. Hire a payroll service.

Signing up with a payroll service will take a lot of weight off your shoulders.

They will do payroll and prepare the payroll taxes that must be filed quarterly with the IRS and the state.

3. Look into opening a self-employed 401k.

Opening a self-employed 401k for your retirement savings is highly recommended.

As a self-employed person, you must take the initiative to save for retirement.

How are corporations taxed?

The corporation will file a corporate tax return instead of filing a Schedule C and reporting any net loss or profit on your federal tax return.

C corporations pay taxes on corporate profits and file with IRS Form 1120.

S corporations don’t pay taxes at the corporate level but still file a federal tax return with IRS Form 1120S.

Profits from S corporations are passed through to the shareholders.

The tax information is reported on Schedule K-1 and has everything you need for your federal tax return.

Tax benefits

As a necessitating business owner, your income will come from a salary or dividends from the corporation’s profits, and you can benefit from various tax deductions.

As a sole proprietor, you can’t deduct any salary you pay yourself, but after incorporating, compensation can be deducted by the corporate entity.

Shareholders pay tax on their compensation, the distribution of dividends by a C corporation, or pass-through profits from an S corporation on their return.

Self-employment tax liability

With a C corp, you are an employee, so you don’t pay any self-employment tax. The corporation pays the employer’s share of the tax for self-employment.

With the S corp, you’ll pay self-employment tax on your salary but not the distributions.

Tax deductions

If you’re incorporated, you can also take advantage of many tax deductions for business expenses.

With a corporation, the actual expenses of running your business can be deducted from your business income.

This alone can reduce your business’s tax liability significantly.

How can you simplify the incorporation process?

You can simplify the incorporation process by using incorporation services to streamline expense tracking for tax deductions, document management, and ensuring compliance with financial regulations.

Here’s how.

Shoeboxed - ideal for small business owners looking to incorporate

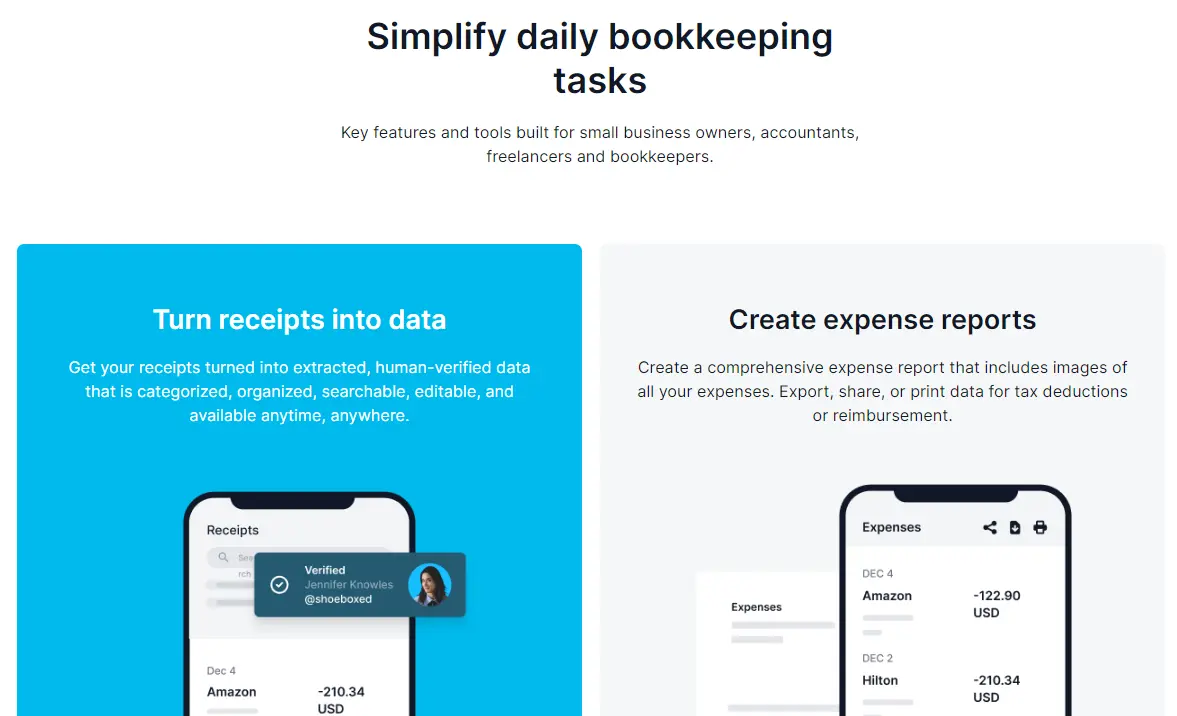

Streamlining involves the automation of expense tracking. Shoeboxed turns your receipts into digital data with automatic data extraction for expense reporting, tax prep, and more.

Automation involves scanning and digitizing.

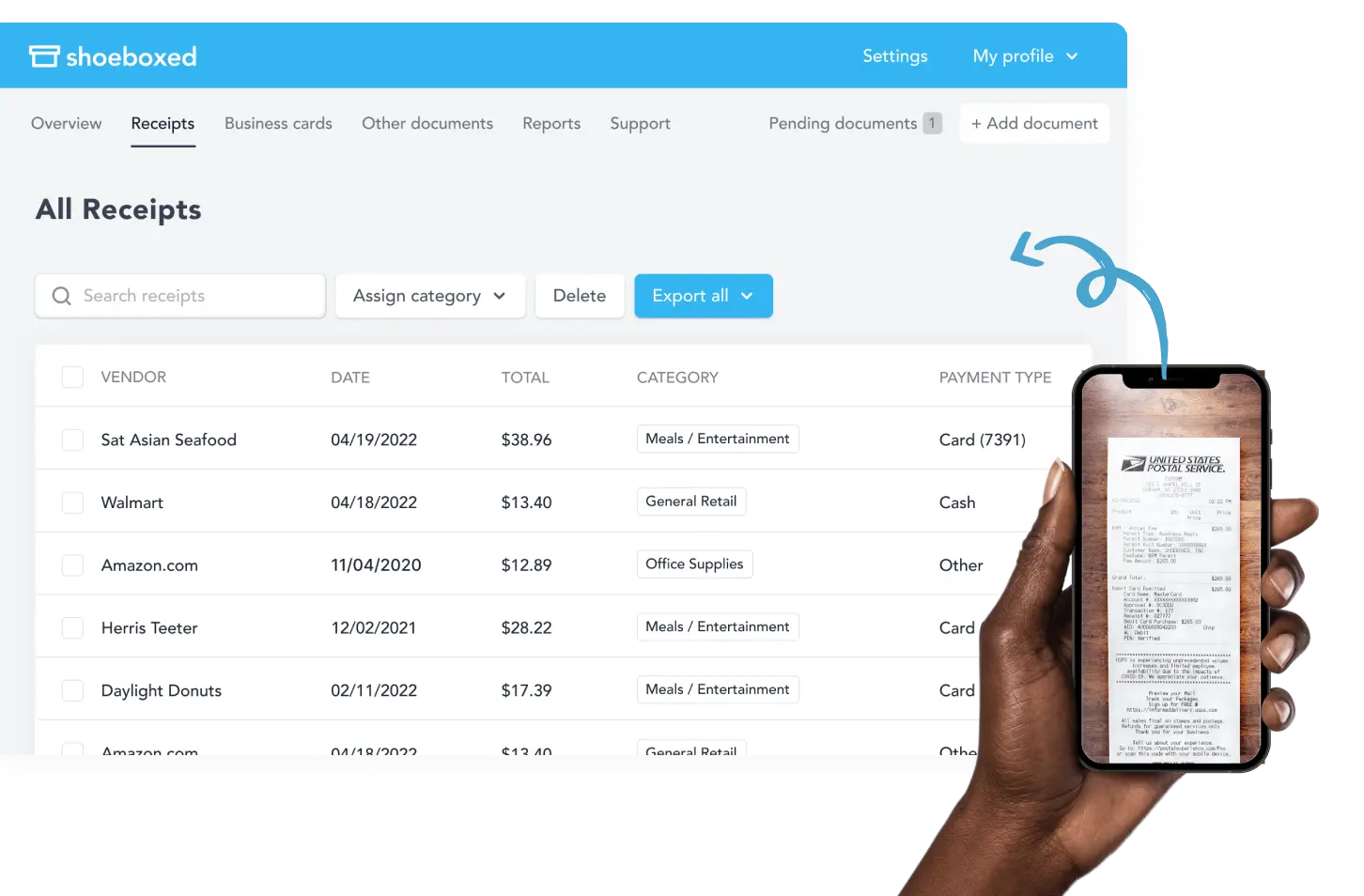

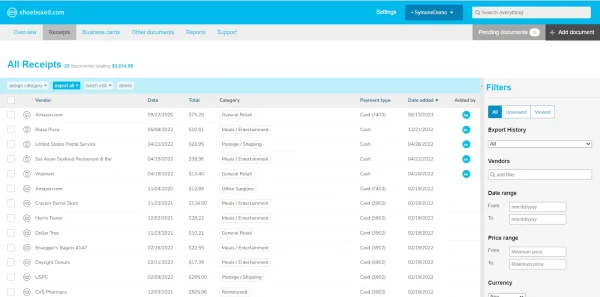

Receipt and document management

Use Shoeboxed for document management to digitize and organize all incorporation-related documents, including receipts for filing fees, legal services, and other expenses. This helps keep all your essential documents in one place.

Shoeboxed allows users to digitize their receipts by taking photos with their mobile devices and uploading them to a designated Shoeboxed account using the app.

That way, all critical documents are securely stored in the cloud, ensuring they are easily accessible and safe from physical damage or loss.

If you don’t have time to scan, you can outsource your scanning to Shoeboxed. Just fill up a pre-paid envelope with a batch of receipts and mail it to Shoeboxed’s processing center. Their team will scan, human-verify, and upload receipts directly to your account.

You can also forward receipts directly from your inbox to your Shoeboxed account, use Shoeboxed’s Gmail plug-in to auto-import e-receipts from your inbox to your Shoeboxed account or drag and drop receipts into the cloud using a desktop or laptop.

Break free from paper clutter ✨

Use Shoeboxed’s Magic Envelope to ship off your receipts and get them back as scanned data in a private, secure cloud-based account. 📁 Try free for 30 days!

Get Started TodayExpense tracking and reporting

Once receipts are uploaded into your account, Shoeboxed automatically extracts vital information (date, amount, vendor) and categorizes the expenses into 15 tax or customized categories, making it easy to generate expense reports.

Shoeboxed will automatically categorize expenses related to incorporation, such as filing fees, legal consultations, and other startup costs.

Turn receipts into data with Shoeboxed ✨

Try a systematic approach to receipt categories for tax time. Try free for 30 days!

Get Started Today

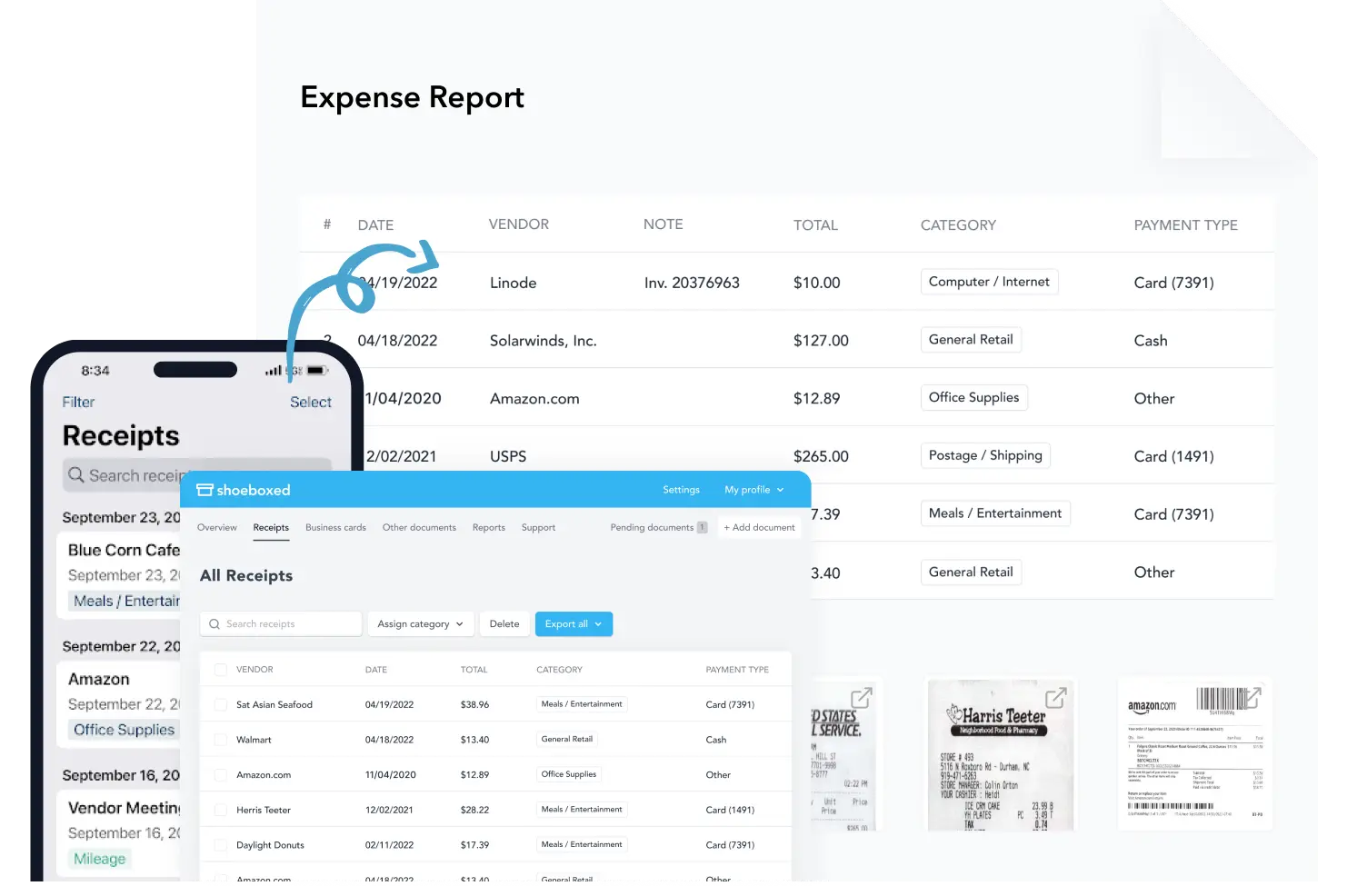

Users can automatically generate expense reports with a click of a button directly from Shoeboxed, customized to meet their organization’s specific needs.

Generate detailed expense reports to provide clear insights into your spending, which is essential for the incorporation of budgeting and financial planning.

Compliance and tax preparation

Shoeboxed stores receipts in a format accepted by the IRS, simplifying tax preparation and ensuring incorporation compliance.

Shoeboxed maintains a digital archive of all receipts and expense reports, creating a clear audit trail for financial transparency and regulatory compliance.

The platform maintains organized financial records, crucial for complying with state and federal regulations. This includes tracking and reporting deductible expenses.

Integration with accounting software

Shoeboxed integrates seamlessly with widespread accounting software like QuickBooks, Xero, and Wave. This allows users to import and categorize expenses easily, reducing manual entry and ensuring that your financial data is accurately recorded and synchronized across platforms.

Incorporating yourself can provide significant advantages for your business but involves detailed steps and compliance requirements. Using Shoeboxed to manage your financial documents and expenses can streamline the process, ensuring you stay organized and compliant.

By leveraging Shoeboxed’s capabilities, you can focus more on growing your business and less on the administrative burdens of incorporation.

Turn receipts into data for tax time ✨

Try Shoeboxed’s systematic award-winning approach to receipt tracking for tax season. Try free for 30 days!

Get Started TodayWhat are some other benefits of incorporating yourself?

Other than tax savings, incorporating yourself has other big business benefits.

1. Liability protection

When you incorporate, you add a layer of limited liability and legal protection between your assets and your business activities.

When you incorporate yourself, you create a separate legal entity for your business from your personal affairs.

2. Lenders are more likely to work with corporations.

Most lenders are more comfortable dealing with a corporation than a sole proprietor because corporations often have established business credit.

This is because corporations have more options to pay off debt.

3. Easier to raise capital

Corporations can issue stock, which is an easy way to raise capital.

4. Looks better for your business

Corporations are seen as more stable and have a more substantial business reputation than sole proprietors or unincorporated businesses.

Individuals feel more secure and comfortable dealing with a corporation than a sole proprietorship because corporations tell them they’re in it for the long haul.

5. Unlimited life

Corporations have perpetual existence. They can exist forever, even if the shareholders die or leave the company.

What are the annual corporate requirements?

There’s much to consider when incorporating your business, including the annual requirements. These requirements include filing tax returns, filing an annual report, and conducting annual meetings.

1. Filing tax returns

Since S corps are pass-through entities, no tax on the business return will be due, but a federal tax filing must still be completed. Depending on the state, you may also need to file a state return.

2. Filing an annual report

You will also need to file an annual report with the state. This keeps business records regarding management and ownership up to date. Some states require an annual report every year, others every other year.

3. Annual meetings and minutes

Annual meetings and minutes are required at the federal and state levels. These don’t need to be filed with the state but must be kept on file. Information regarding annual meetings and minutes may be required if the business is audited, along with other tax documents.

Frequently asked questions

What does it mean to incorporate yourself?

Incorporation creates a separate business entity that separates your business from your personal affairs. This is one way to protect your personal assets.

Why would an individual incorporate?

Individuals can gain incorporation benefits by separating their business activities from their assets and finances. Incorporating limits personal liability and can save on taxes.

How is a business owner paid when incorporated?

Business owners are paid either a salary or dividends from the profits.

Are lenders more likely to work with a sole proprietorship or a corporation?

Most lenders are more comfortable dealing with corporations than sole proprietorships because corporations often have better access to business credit. This is because corporations have more options to pay off debt.

In conclusion

Incorporating yourself can provide significant advantages for your business but involves detailed steps and compliance requirements. Using Shoeboxed to manage your financial documents and expenses can streamline the process, ensuring you stay organized and compliant. By leveraging Shoeboxed’s capabilities, you can focus more on growing your business and less on the administrative burdens of incorporation.

Caryl Ramsey has years of experience assisting in bookkeeping, taxes, and customer service. She uses various accounting software to set up client information, reconcile accounts, code expenses, run financial reports, and prepare tax returns. She is also experienced in setting up corporations with the State Corporation Commission and the IRS.

About Shoeboxed!

Shoeboxed is a receipt scanning service with receipt management software that supports multiple methods for receipt capture: send, scan, upload, forward, and more!

You can stuff your receipts into one of our Magic Envelopes (prepaid postage within the US). Use our receipt tracker + receipt scanner app (iPhone, iPad and Android) to snap a picture while on the go. Auto-import receipts from Gmail. Or forward a receipt to your designated Shoeboxed email address.

Turn your receipts into data and deductibles with our expense reports that include IRS-accepted receipt images.

Join over 1 million businesses scanning & organizing receipts, creating expense reports and more—with Shoeboxed.

Try Shoeboxed today!