Travel Expense Report Template (Google Sheets) for Business Trips

Free Google Sheets travel expense report template for self-employed people. Copy it to your Drive, log your trip, get a clean tax-ready total. Plus the per-diem method almost nobody uses.

Most travel expense templates bury you in receipts and skip the IRS rules. I built this one in Google Sheets so you don’t have to think about either. Copy it to your Drive, log your trip, and walk away with a clean number for Schedule C or for your accountant.

What you get: a Google Sheets travel expense report you can copy and edit in your Drive.

What it tracks: hotel, flights, ground transport, meals (with the 50% rule baked in), per-diem days, and mileage to and from the airport.

What it answers: what the IRS counts as a deductible business trip, and how to keep records the way Pub 463 wants.

Heads up: fly somewhere for work, tack on a Saturday on the beach or a Sunday with family, and you can still write off the round-trip flight. The trick is the trip has to be mostly for work. There’s a whole section below with the IRS rules for doing this the right way.

Get the travel expense report template

Copy the template to my Google Drive →

Prefer a different format? Download as Excel (xlsx)

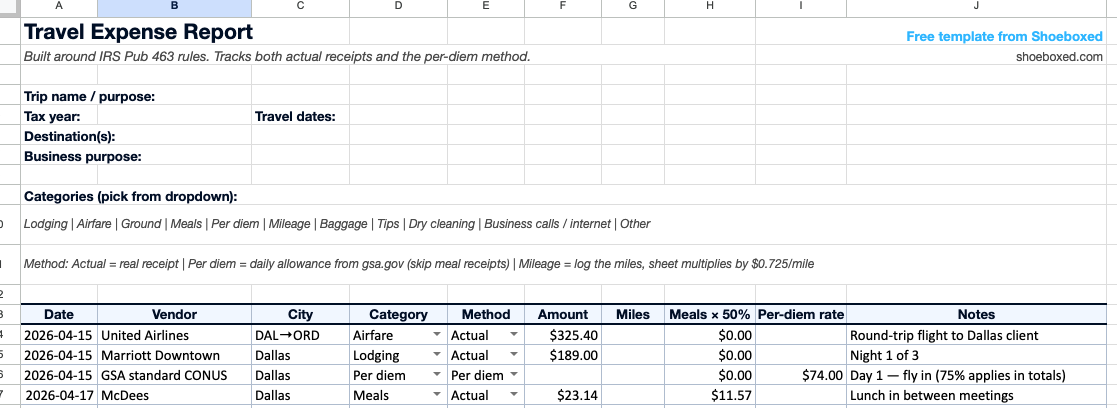

The template has ten columns. Each one earns its place.

Date: the day of the expense, so the totals line up by trip and by year. Vendor: who you paid, like United, Marriott, Uber, or the steakhouse you took the client to. City: where you spent the money, which matters most when you switch to the per-diem method below. Category: Lodging, Airfare, Ground, Meals, Per diem, Mileage, or Other. Method: Actual (a real receipt), Per diem (the daily rate, explained below), or Mileage (logged miles at the IRS rate). Amount: what the receipt says, including tax and tip. Miles: the trip distance, if Method = Mileage; the sheet multiplies by the 2026 business rate of $0.725 a mile. Meals × 50%: the sheet does the math for any Meals row, because the IRS only lets you deduct half. Per-diem rate: the daily rate from gsa.gov for that city, if you picked Method = Per diem. Notes: trip purpose, client name, and anything else you’ll want to remember at tax time.

The bottom of the sheet adds it all up. The number on the bottom-right is what goes on Schedule C, line 24a (Travel) and 24b (Meals × 50%).

If you only do one thing on this page, copy the template. The rest of this article is for when you want to know what the IRS rules say.

What counts as a business travel expense

The IRS lets you deduct travel expenses when you’re away from your tax home for work, and two of those words trip people up.

Your tax home isn’t your house, it’s your regular place of business. IRS Publication 463 defines it like this:

Generally, your tax home is your regular place of business or post of duty, regardless of where you maintain your family home. It includes the entire city or general area in which your business or work is located.

In plain English: if you work from a home office in Wilmette and fly to Dallas for a client meeting, Dallas is “away from home.” The trip is deductible. If you live in Wilmette but commute every day to an office in downtown Chicago, your tax home is Chicago, not Wilmette. A drive to a client in the western suburbs from your Chicago office is travel; the drive between Wilmette and downtown Chicago is commuting and not deductible.

The other tripwire is the one-year rule. If you take a temporary assignment somewhere that you reasonably expect to last one year or less, your tax home doesn’t change. You can deduct the travel the whole time. If the assignment is realistically expected to last more than a year, the new city becomes your tax home and you can’t deduct the travel anymore.

That’s the foundation. Once you’re legitimately “away from your tax home for business,” everything below is in play.

Hotel, flight, ground transport, and baggage

These are the obvious deductible categories. Most of the template’s rows will land here.

Lodging: hotel, motel, or Airbnb at your actual cost, and always keep the receipt because there’s no shortcut method for lodging. Flights, trains, buses: the actual cost to get from your tax home to your destination and back, deductible in full. Rental car, taxi, Uber, Lyft: transportation around your destination plus the ride from your house to the airport and back, all deductible at actual cost. Baggage and shipping: checked bag fees, plus shipping samples or display materials to a conference if you need them at the other end. Tips: what you hand to porters, hotel staff, and drivers along the way (these count even though they rarely come with a receipt). Dry cleaning and laundry: the IRS rolls these into the trip cost if your trip is long enough to need them. Business calls and internet: WiFi on the plane, an extra hotspot day, or a business call from your hotel room.

Log each one in the template under Category, and set the Method column to Actual for everything here.

Meals are different because of the 50% rule, and they get their own section next.

Meals on a business trip (and the 50% rule)

When you eat out on a business trip, can you deduct the whole bill? No. You deduct half. That’s the 50% rule, and it applies whether you’re alone or with a client.

The IRS says it like this in Pub 463:

If you aren’t reimbursed, the 50% limit applies even if the unreimbursed meal expense is for business travel.

So a $40 client dinner becomes a $20 deduction. A $1,400 week of meals across a 5-day trip becomes a $700 deduction. The template’s Meals × 50% column does this math for you. Enter $40 in the Amount column for a Meals row and $20 lands in the deduction column.

A nice surprise: the IRS isn’t trying to make you eat at the diner. Pub 463 has a clean line on this:

Meal expenses won’t be disallowed merely because they are more than a fixed dollar amount or because the meals take place at deluxe restaurants, hotels, or resorts.

Take the client to the steakhouse if it’s reasonable for the relationship. Just deduct half.

There’s a faster way to handle meals that almost nobody knows about. It’s next.

Skip the meal receipts. Use the daily allowance.

When you travel for work, the IRS gives you two ways to write off meals.

Way 1: Save every meal receipt, add them up, and deduct half of the total. Way 2: Skip the receipts, use the daily meal rate the government already set for your city, and deduct half of that.

Way 2 is called the per diem method. It’s right there in IRS Pub 463:

You can use the standard meal allowance whether you are an employee or self-employed, and whether or not you are reimbursed for your traveling expenses.

It takes about thirty seconds. And out of 1,409 self-employed travelers in our Shoeboxed customer data over the last two years, only 234 receipts were tagged with a per-diem rate. That’s 0.2%. Almost nobody does this.

Here’s how Way 2 works

You’re going to Dallas for a 3-day client meeting.

The IRS publishes a simplified two-tier daily meal rate every year: one number for most cities, a higher number for expensive ones (the official name is the “high-low” method). For trips through September 2026, it’s $74 a day for most cities and $86 a day for high-cost places like New York, San Francisco, or Boston (IRS Notice 2024-68). Dallas falls in the $74 group.

So the math:

- Pull the rate. Dallas = $74 a day.

- Multiply by days. $74 × 3 = $222.

- The IRS limits business meals to 50% no matter which method you use. $222 × 50% = $111 deduction.

No receipts, and no adding up your $9 breakfast, $14 sandwich, and $42 dinner.

| Day | What happens | Math | Per-diem |

|---|---|---|---|

| Day 1 | Fly in | $74 × 75% | $55.50 |

| Day 2 | Full day | $74 | $74.00 |

| Day 3 | Fly home | $74 × 75% | $55.50 |

| Total per-diem | $185.00 | ||

| Apply the IRS 50% meals rule ($185 × 0.50) | = $92.50 | ||

| Schedule C deduction | $92.50 | ||

Want a city-specific rate instead of the simplified high or low? Look up your destination at gsa.gov/perdiem. Some cities run higher than $74 but lower than the $86 high-cost flat. Either method works for self-employed travelers. If you don’t want to bother, default to the $74 / $86 high-low — it’s the simpler one and lands within a few dollars of the city-by-city rate for most destinations. Pick one method and use it consistently for the year.

One thing you DO still have to log

You don’t need a receipt for every $9 breakfast, but you DO still need to log the per-diem days in the template (or in whatever record you use). One row per day at the daily rate. That’s the record the IRS wants if anyone asks: dates of travel, destination, business purpose, and the rate you claimed. The template’s Per-diem rate column plus the Notes column give you all four.

The receipts get skipped, but the log doesn’t.

What still needs a receipt

Hotels. Pub 463 is direct on this:

There is no optional standard lodging amount similar to the standard meal allowance. Your allowable lodging expense deduction is your actual cost.

The per-diem method only covers meals, so hotel costs still come off your actual receipts. There’s no shortcut for lodging.

The travel-day catch

What about the day you fly in or out? You only get 75% of the daily rate, because you weren’t there for all three meals. The 3-day Dallas trip rebuilt with the catch baked in:

- Day 1 (fly in): $74 × 75% = $55.50

- Day 2 (full day): $74

- Day 3 (fly home): $74 × 75% = $55.50

- Total: $185 × 50% = $92.50 deduction

Five minutes of math. Zero meal receipts. The template’s Per-diem rate column is where you log the rate; the Method column flips to “Per diem” and the sheet handles the rest.

How to mix business and vacation (the legal way)

The IRS lets you tack personal days onto a business trip and still write off the round-trip flight. Here’s exactly when, with three real IRS examples translated from Pub 463.

Rule 1: The trip has to be PRIMARILY business

What does “primarily business” mean? It means the main reason you got on the plane was to work.

You fly from Atlanta to New Orleans for 6 days of client meetings. On your way home, you stop in Mobile for 3 days to visit your parents.

That’s allowed. The IRS itself uses this exact example. You can deduct:

- 100% of the round-trip flight (the meetings were the primary reason for going)

- 100% of the New Orleans hotel and meals (the 6 business days)

- $0 for the Mobile detour (the 3 personal days)

The IRS’s own numbers: 9 total days cost you $2,165. Without the Mobile stop you’d have been gone 6 days at $1,633.50. You deduct $1,633.50.

| Leg of the trip | Days | Deductible? | $ |

|---|---|---|---|

| Round-trip flight Atlanta → New Orleans → Atlanta | — | 100% deductible | in |

| Hotel + meals in New Orleans (business) | 6 days | Deductible | in |

| Mobile detour to visit parents (personal) | 3 days | Not deductible | out |

| Total trip cost | — | $2,165.00 | |

| Deductible portion | $1,633.50 | ||

How you lose the deduction: flipping the ratio. Fly to New Orleans for 3 days of meetings and stay 6 days at the beach? Now the trip is primarily personal. You lose the flight write-off entirely.

Rule 2: Weekends in the middle count as business days

Client meeting in Quebec on Friday, another one Monday, and you sightsee Saturday and Sunday in between.

All four days count as business days. Hotel and meals deductible Friday through Monday, including the weekend you spent sightseeing.

The IRS calls this the “sandwich rule.” Weekends sandwiched between business days count because flying home for 48 hours doesn’t make sense. Pub 463 spells it out:

Count weekends, holidays, and other necessary standby days as business days if they fall between business days.

| Day | What you did | Why it counts | Deductible? |

|---|---|---|---|

| FRI | Client meeting | Business day | ✓ |

| SAT | Sightseeing | Sandwiched between business days | ✓ |

| SUN | Sightseeing | Sandwiched between business days | ✓ |

| MON | Client meeting | Business day | ✓ |

How you lose the deduction: if your Monday meeting cancels and you decide to stay through Sunday for fun, Saturday and Sunday flip to personal days. The rule needs the business meeting on the back end.

Rule 3: Your spouse’s costs don’t deduct (with one exception)

You drive to Chicago for a 3-day conference and bring your spouse. The hotel is $199 a night for a double room. A single would have been $149.

You deduct $149 a night, and the $50 difference is on you.

You can still deduct the full driving cost because you were driving anyway. Pub 463 is direct about this:

If a spouse, dependent, or other individual goes with you (or your employee) on a business trip or to a business convention, you generally can’t deduct their travel expenses.

The exception: if your spouse is on your payroll AND has a real business reason to be there (not “they helped with notes at dinner”), their costs can deduct too. For most owner-operators, that’s not the situation, so plan to eat the incremental cost of the second person.

One footnote for foreign trips

If you’re abroad more than a week, the rules tighten. Less than 25% of your total time can be personal, or you have to split the airfare proportionally. Domestic trips don’t have that 25% threshold. If you’re flying overseas with vacation days bolted on, read Pub 463’s “Travel Outside the United States” section before you book.

Don’t bolt a meeting onto a vacation

The IRS sees through this one. Pub 463 says it plainly:

A trip to a resort or on a cruise ship may be a vacation even if the promoter advertises that it is primarily for business.

If the trip is mostly personal and you set up one meeting to justify deducting the flight, you’ll lose the deduction in an audit. The fix is to document the business reason BEFORE you go: calendar invites to clients, emails confirming meetings, the conference registration. That’s the paper trail that proves “primarily business” if anyone asks. The template’s Notes column is the right place to keep that record alongside the trip.

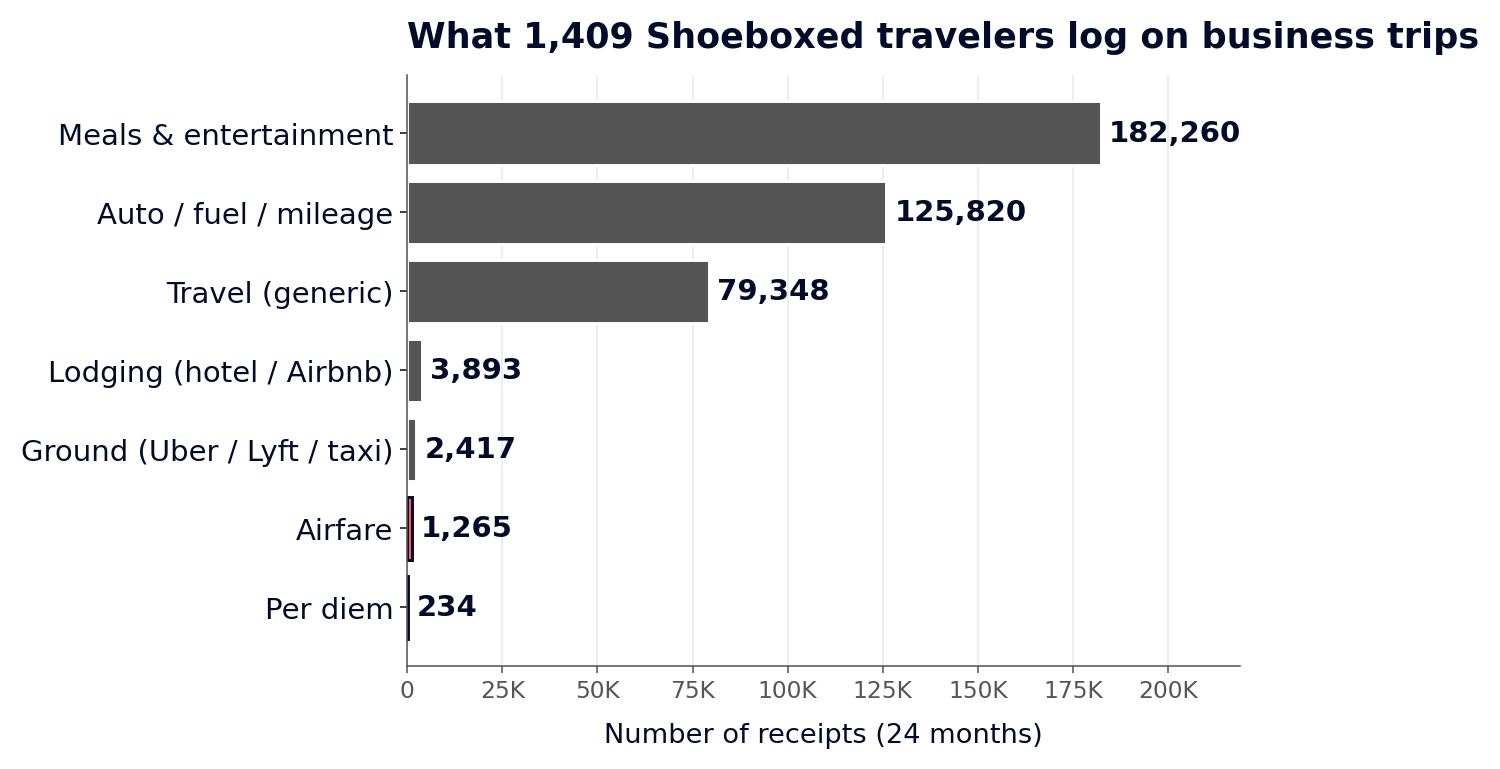

What 1,409 Shoeboxed customers log on business trips

Here’s something I see in our customer data that took me by surprise.

We pulled 24 months of receipts from 1,409 Shoeboxed accounts that scan at least 10 travel-category receipts a year. That’s 1.1 million receipts total across these accounts. Of those, 107,349 carry an explicit travel-related category tag.

If you slice the same 1.1 million receipts by what they’re tagged as (meals, mileage, lodging, and so on), the totals look like this:

- Meals and entertainment: 182,260 receipts

- Auto / fuel / mileage: 125,820 receipts

- Travel (generic): 79,348 receipts

- Lodging (hotel / Airbnb): 3,893 receipts

- Ground (Uber / Lyft / taxi / rental): 2,417 receipts

- Airfare: 1,265 receipts

- Per diem: 234 receipts

- No category at all: 289,264 receipts (25.7% of the cohort)

(Categories overlap with the “travel” bucket because a meal-tagged receipt on a trip lives in both lenses. The numbers above don’t add to 107,349; they’re the full-cohort breakdown.)

Three things jumped out.

First, per diem is 0.2% of travel receipts. That’s why the per-diem section above exists; almost nobody uses the standard meal allowance even though the IRS has offered it for decades.

Second, airfare is dramatically under-captured. 1,265 airfare receipts across 1,409 travel-active accounts works out to less than one flight scanned per account every two years. That can’t be right; these are people who travel for work. The flight confirmations are arriving by email and never landing in the receipt system. The lodging-to-airfare ratio is 3 to 1, which is the dead giveaway: people scan the hotel folio when they check out but forget the flight from three weeks earlier.

The fix isn’t more discipline. The fix is to forward booking confirmations to a receipt scanner that pulls them out of Gmail automatically. Shoeboxed Gmail Receipt Sync does this, and the airfare gap closes itself.

Third, one in four receipts has no category at all. That’s harder to defend in an audit because at the end of the year you’re not going to remember why you bought that $46 thing at Walgreens in Tucson. Categorize as you go, even loosely.

Two more deductions worth claiming on every business trip

You know what people miss on travel deductions? The two that sit next to the trip itself: the home office and every business mile you drive.

Home office (simplified method): if you have a dedicated workspace at home, you can deduct $5 per square foot up to 300 square feet. That’s up to $1,500 a year with zero receipts and zero math. The Shoeboxed home office calculator runs the numbers on your address in about thirty seconds.

Every business mile you drive: the IRS 2026 business mileage rate is $0.725 per mile. That covers a lot more than the drive to the airport.

- Drive from your home office to a client meeting across town? Deductible.

- Drive 350 miles to a sales call instead of flying? Deductible.

- Contractor driving to and from a jobsite? Deductible.

- Realtor driving between showings? Deductible.

A 30-mile round trip to O’Hare adds $21.75 to a trip. A 350-mile day on a sales route adds $253.75. Across a year of business driving, mileage is often the single biggest deduction on Schedule C.

The catch is the log. The IRS wants the date, the miles, the destination, and the business purpose for every drive. The Shoeboxed app does this automatically: GPS tracks every drive in the background, and at the end of each day the app texts you the list of trips. You reply with which ones were business (or medical, or charity), and a tax-ready mileage log lands in your Shoeboxed account. No notebook in the glove box, no end-of-year reconstruction. If you’re tracking by hand, log each drive in this template under Method = Mileage and the sheet multiplies by $0.725.

Should the business pay you back?

This trips up most owner-operators, and the answer depends on your business entity.

If you’re a sole proprietor or single-member LLC (Schedule C): you ARE the business for tax purposes. There’s no separate reimbursement game. You pay the expense personally, log it, and deduct it on Schedule C. Mileage goes on Schedule C at $0.725 a mile. No reimbursement.

If you’re an S-corp, multi-member LLC, or corporation: the business is a separate taxpayer, and you can set up something called an accountable plan that pays you back tax-free. Pub 463 spells out the three rules:

- Business connection. The expense has to be ordinary and necessary for the business.

- Adequate accounting within 60 days. You turn in receipts and a mileage log.

- Return any excess advance within 120 days. If the business advanced money and you spent less, you return the difference.

Meet the three rules and the magic happens:

| Path | Business deducts? | You pay tax on the money? |

|---|---|---|

| W-2 wages | Yes | Yes (income tax + payroll tax) |

| Accountable plan reimbursement | Yes | No |

So in an S-corp, you submit a mileage log every month, the company writes you a check at $0.725 per mile, the company deducts it as a business expense, and you pay zero personal tax on the reimbursement. Hotel and meal receipts work the same way: front the cost, submit substantiation, business cuts a check.

Schedule C is simpler, and S-corp is a real tax deal. Either way, the template captures what you spent; the entity structure determines what you do with the total.

How long to keep business travel records

Three years, not seven.

The “keep everything for seven years” folklore is wrong for most people. The IRS’s official answer is three years from the date you filed the return:

Keep records for 3 years if situations (4), (5), and (6) below do not apply to you.

The exceptions push the window longer in narrow cases:

- 6 years if you under-report income by more than 25%.

- Indefinitely if you don’t file a return at all.

- Indefinitely if you file a fraudulent return.

For the vast majority of self-employed travelers, three years is the rule. Keep the scan in your Shoeboxed account or your Drive, toss the paper receipt once the data is captured. Thermal-paper hotel receipts go gray within a year anyway; the scan outlasts the original.

The easy way is to skip the spreadsheet

I bought Shoeboxed late last year for a reason: owning a small business is one of the best tax deals in America, and the messy receipt pile is what stops most people from claiming what they’ve earned. I’d watched it happen to friends, to my own consulting clients, and (for a few years) to myself.

The template works, and it’s all in this article. But the manual entry is the part nobody enjoys, and our customer data shows what happens: flights don’t get logged, categories stay blank, meals pile up unreviewed.

The Shoeboxed app is the same job without the typing. Snap a paper receipt, forward an email, or ship us a shoebox of paper receipts in our Magic Envelope. Our team in Durham scans the paper ones, our software reads each receipt for the key fields the IRS needs (date, total, tax, vendor, expense category), and the data lands in your account ready to use. If you’re lazy like me, turn on Gmail Receipt Sync. It pulls receipts right out of your Gmail, including flight confirmations and online-order receipts, which closes the airfare gap from section 7 without you lifting a finger.

Our Shoeboxed app makes creating mileage receipts a breeze. GPS tracks every drive in the background, so you don’t have to remember to open anything. At the end of each day the app texts you the list of trips, and you reply with which ones were business. That’s it. A tax-ready mileage log lands in your Shoeboxed account: date, miles, IRS rate, total, ready to hand to your accountant. No spiral notebook in the glove box, no January scramble trying to reconstruct a year of driving. (Our deeper writeup of the mileage app, with screenshots, is in the mileage log template article.)

Either way, you get there faster with the receipts already captured.

Shoeboxed Pro is $29 a month, with a 30-day risk-free trial. If you scan your year of travel and decide it isn’t for you, we refund the money.

Start a Shoeboxed account → or get the iPhone app or the Android app.

Let’s go get it.

Helping you keep more of your hard-earned money is the whole point.

Tracking your whole business, not just trips? Our Google Sheets accounting template rolls income and expenses into a Schedule C profit and loss statement.

Renting out a place on Airbnb? Our Airbnb expense spreadsheet maps every host expense to its Schedule E line.

Wondering whether the per diem itself gets taxed? Here's when per diem is taxable and the receipt rule that keeps it tax-free.

Work From Home? You Could Be Missing $500–$3,000/Year

Self-employed, 1099, or freelancer? Enter your address and we'll pull your real property data to estimate your home office deduction.

Free · 30 seconds · No signup required