Bank Transaction Receipt: What It Is + When Your Business Needs One

A bank transaction receipt is the slip your bank hands you when money moves. See a real example with every field labeled, learn when a statement can replace it, and find out how long to keep yours.

Updated June 2026.

A bank transaction receipt is the slip or confirmation your bank gives you when money moves: a deposit, a withdrawal, a transfer, or a payment. It shows the date, the amount, the transaction type, part of your account number, and a reference number the bank can use to find the transaction again.

Imagine you're walking out of the bank after depositing two client checks. The teller hands you a slip, and by Friday it's riding around in the cupholder. Keep it or toss it? Keep it. That slip is one of the documents the IRS names for proving your business income. Keep reading to see why, and to learn when the statement in your bank app can stand in for it.

I am Doug. I own Shoeboxed, and since 2007 we have scanned over 57 million receipts for more than 552,000 small businesses. Bank receipts turn out to be the rarest paper in the pile, and I have the numbers to prove that below.

What a bank transaction receipt is

Any time money moves through your bank account with you standing there, the bank offers you a record of it. The teller prints a slip after a deposit. The ATM spits one out after a withdrawal, and the app emails a confirmation after a transfer. All of those are bank transaction receipts, and most people shorten the name to bank receipts.

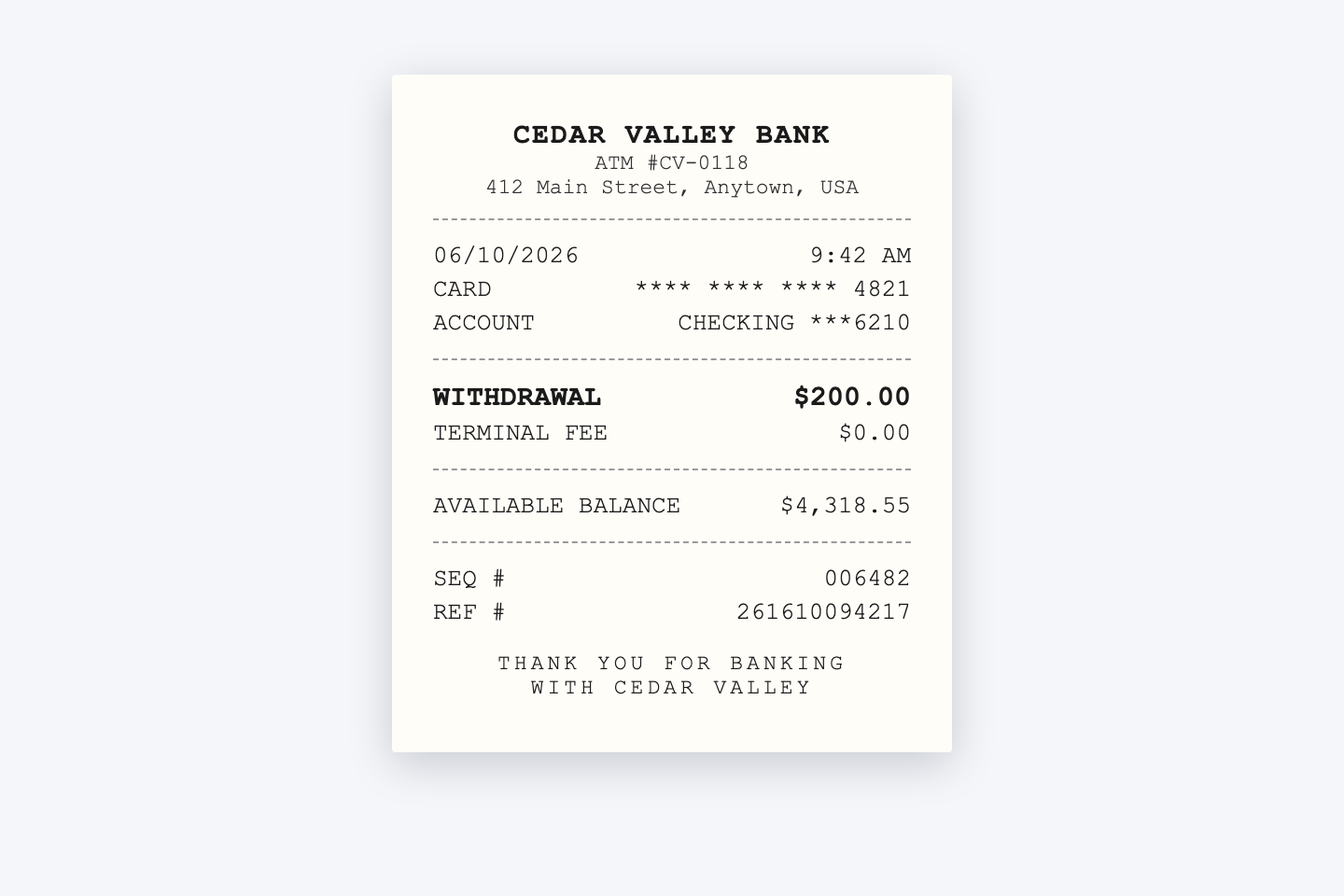

A typical ATM withdrawal receipt. Date, amount, account, and reference number, all on one slip. (Cedar Valley Bank is made up for the example.)

A typical ATM withdrawal receipt. Date, amount, account, and reference number, all on one slip. (Cedar Valley Bank is made up for the example.)

A bank receipt differs from the store receipts in your pile in one useful way. A store receipt proves you bought something, and a bank receipt proves money moved between accounts. Deposits, withdrawals, wire transfers, loan payments, and cashier's checks all produce one. Store receipts go by a few names of their own, sales receipt and transaction receipt among them, and our types of receipts guide sorts them all out.

Paper or digital makes no difference. An emailed transfer confirmation proves as much as the teller's slip, the same way an e-receipt proves as much as a register tape.

What's on a bank receipt

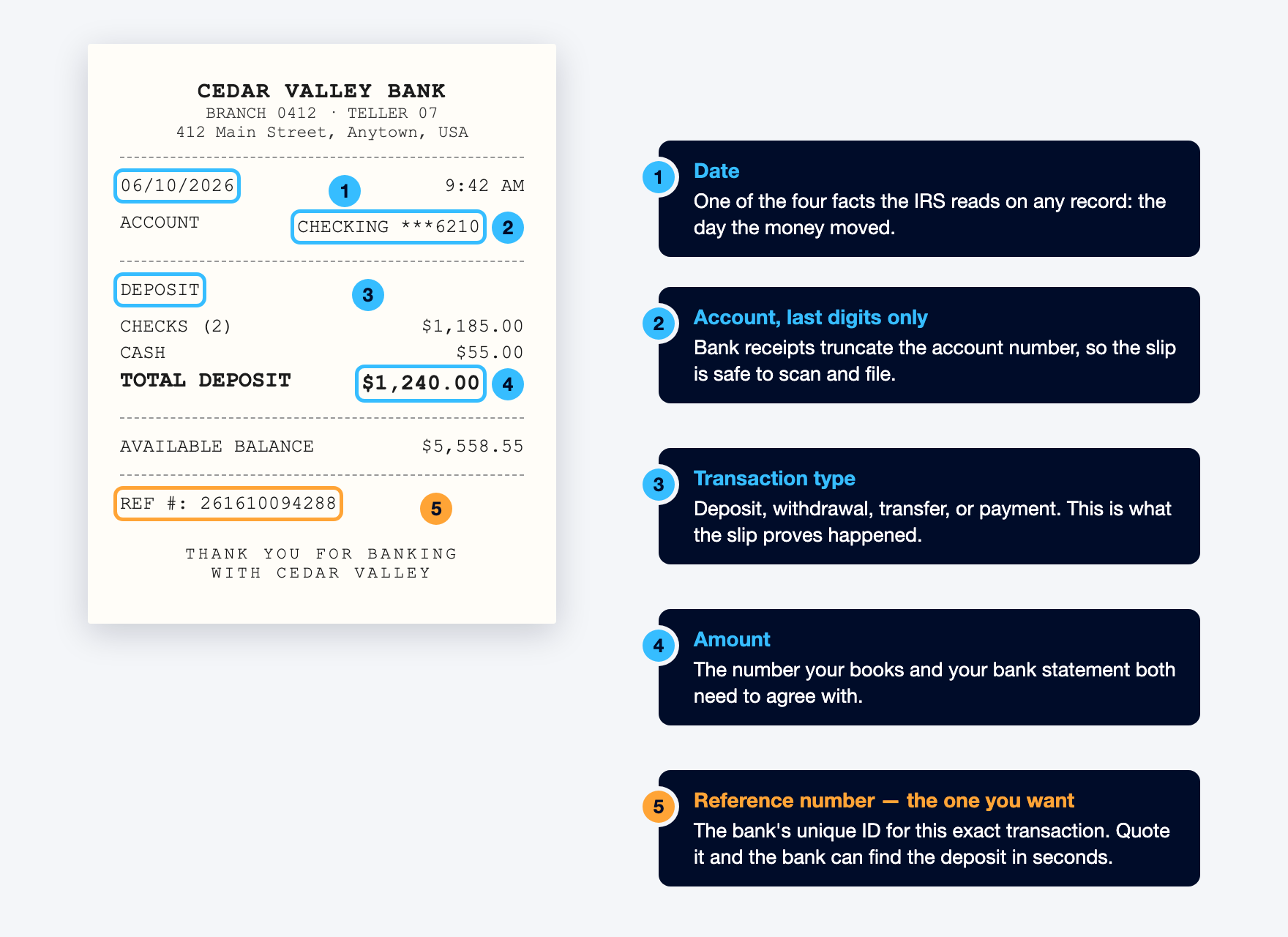

Strip away the logo and every bank receipt carries the same handful of fields. Here is a teller deposit slip with everything labeled.

Where everything lives on a bank deposit receipt. The reference number, labeled in orange, finds this exact transaction again. (Cedar Valley Bank is made up for the example.)

Where everything lives on a bank deposit receipt. The reference number, labeled in orange, finds this exact transaction again. (Cedar Valley Bank is made up for the example.)

That list of fields lines up with the test the IRS applies to any record, straight from Publication 463:

"Documentary evidence will ordinarily be considered adequate if it shows the amount, date, place, and essential character of the expense."

IRS, Publication 463

Amount, date, place, and what it was. A bank receipt shows all four: the dollar figure, the day, the bank, and the transaction type. The reference number is the bonus field. The IRS never asks for it, but quote it to the bank and they'll pull up that exact deposit while you wait. That beats describing "a deposit sometime in March, maybe $1,200."

One worry I can mostly take off your plate: bank slips show only the last few digits of your account, not the full number. A slip fished out of the trash won't get anyone into your checking account, so it's safe to scan, file, and hand to your bookkeeper.

Bank receipt vs. bank statement: which one does the IRS want?

People ask me this one all the time, usually in April. The receipt is the slip for one transaction, and the statement is the month's list of all of them. For proving a payment happened, the IRS takes either, and Publication 583 spells out when a statement works. If you paid by electronic transfer, the statement must show the amount, who you paid, and the date the transfer posted. A screenshot of the confirmation counts too, as long as it shows those three things. Pub 583 adds one catch worth reading twice:

"Proof of payment of an amount, by itself, does not establish you are entitled to a tax deduction."

IRS, Publication 583

The statement proves you paid, but it doesn't prove what you paid for. The tax man wants the bill or itemized receipt alongside it. Pub 463 says the same thing about checks: a canceled check plus the bill it paid proves the cost, but a canceled check alone doesn't prove a business expense. Here is the practical split.

| Bank receipt | Bank statement

---|---|---

Covers | One transaction | A month of transactions

You get it | On the spot, at the teller or ATM | Monthly, in the app or the mail

Best at proving | A specific deposit or payment happened, with a reference number to trace it | The pattern of money in and out, for balancing your books

Works for the IRS? | Yes | Yes, if it shows the amount, who you paid, and the posting date, with the bill for deductions

What it can't do | Show the rest of the month | Prove what an expense was for, without the bill or receipt

If you balance the books monthly, you'll use both. The statement is the checklist, and the slips and receipts are the proof behind each line.

Do banks even hand out paper receipts anymore?

Yes. Under Regulation E, the bank must make a receipt available for any electronic transfer you start at an ATM or terminal. Regulation E makes one exception: transfers of $15 or less. The slip is your legal right, which is why the machine keeps asking.

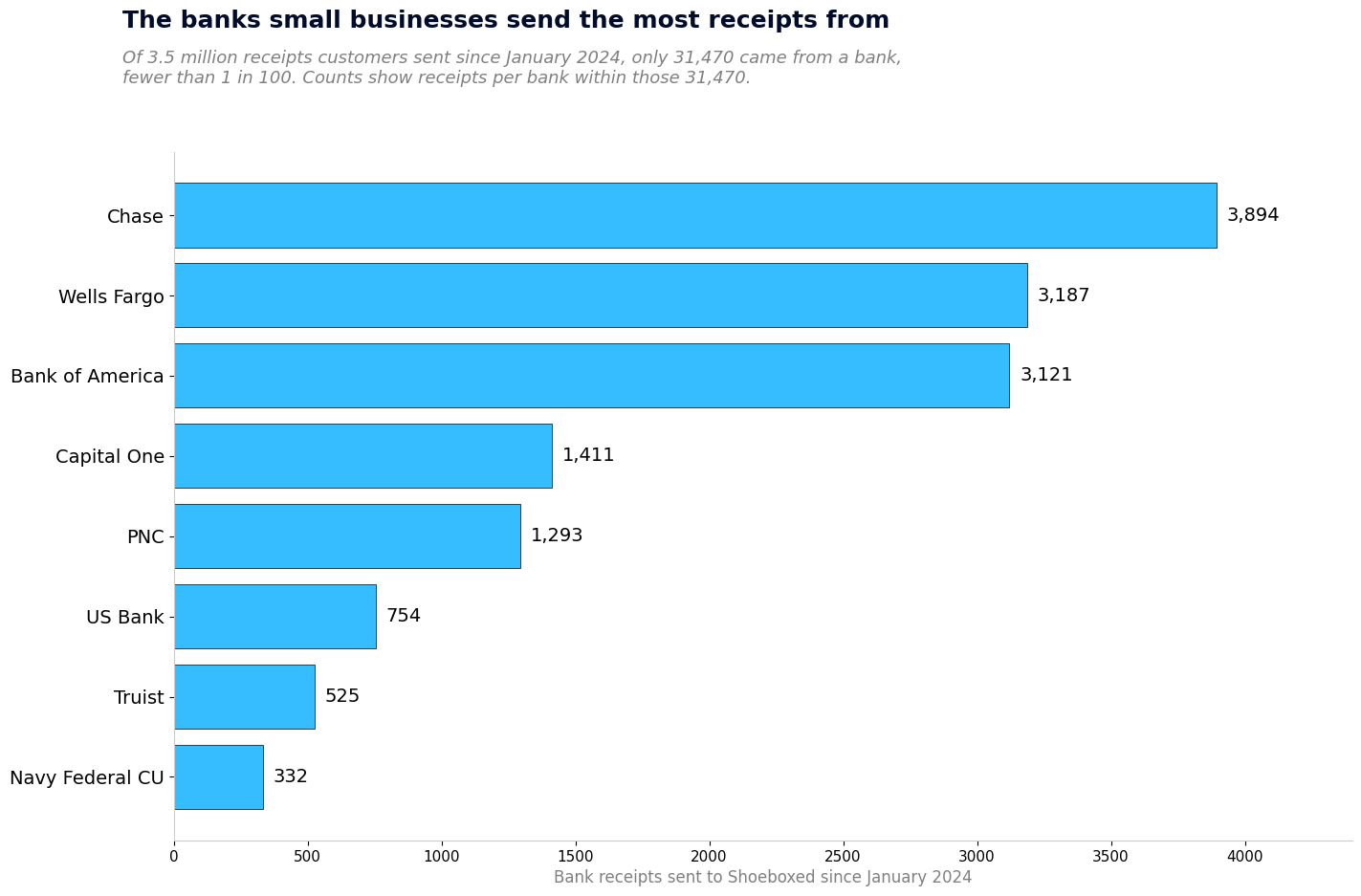

Whether anyone keeps those slips is another story, and our scanning pile answers it. If we zoom out across the 3.5 million receipts customers sent us since January 2024, only 31,470 came from a bank or credit union. That's fewer than 1 in 100. The paper bank receipt is the rarest slip in the small-business pile, because banking moved into the app and the statement quietly took over the proof-keeping job.

The banks behind the 31,470 bank receipts customers sent us since January 2024. Chase, Wells Fargo, and Bank of America top the list.

The banks behind the 31,470 bank receipts customers sent us since January 2024. Chase, Wells Fargo, and Bank of America top the list.

The 1,744 businesses that do send us bank receipts skew toward the big banks. Chase, Wells Fargo, and Bank of America cover about a third of the pile between them. Most of those slips get filed under a bank or ATM category. About 1 in 5 arrive with no category at all, and some of those are slips too faded to read.

Why bank receipts matter at tax time, and how long to keep them

Most receipt advice obsesses over deductions. An audit checks both directions, though, and bank receipts earn their keep on the income side. Publication 583 names them outright:

"You should keep supporting documents that show the amounts and sources of your gross receipts. Documents that show gross receipts include the following. Cash register tapes. Bank deposit slips. Receipt books. Invoices. Credit card charge slips. Forms 1099-MISC. Forms 1099-NEC."

IRS, Publication 583

Bank deposit slips sit second on the list. Say your Schedule C reports $48,000 of income, but $52,000 landed in your checking account that year. The IRS will want to hear about the extra $4,000. Deposit slips with your own notes let you show it was a tax refund and a loan from your brother, not unreported sales. The slip that proves a deposit was NOT income can save you more grief than any expense receipt in the pile.

So how long do you hang on to them? Here is how far back the IRS can look:

| Your situation | Keep records for |

|---|---|

| A normal tax return | 3 years |

| You left off more than 25% of your income | 6 years |

| You claimed a loss for a bad debt or worthless stock | 7 years |

My rule for most small businesses: keep everything seven years and never think about it again. The catch is the slip itself. ATM receipts come off the same fading thermal paper as register tape, and a faded slip proves nothing. Get the image saved before the ink gives up. For what the IRS expects any receipt to show, here are the IRS receipt requirements.

How to get a bank receipt, or a copy of one

Getting one in the moment is the easy part, because the teller and the ATM hand them out on the spot. For transfers and bill payments inside the app, tap the transaction, look for a confirmation or receipt button, and save the PDF or a screenshot.

Lost the slip? Call the bank or walk into a branch. Give them the date and amount, or the reference number if you saved it anywhere, and they'll reprint a transaction record. For older transactions, ask for a copy of the statement that covers that month. Most banks keep several years of history, though some charge a fee to dig up a single old transaction. Here is what to do about a lost receipt while you wait.

The path I'd pick: keep your own copy automatically, so the bank's records become your backup instead of your only hope. That's the problem Shoeboxed was built to solve. Send us a bank slip and we store the actual image. Our software pulls out the bank, the date, and the amount, the fields the IRS wants to see. You can get them in five ways:

- Snap a picture in the app before the slip leaves the cupholder.

- Drop the paper in a prepaid Magic Envelope and mail it to us.

- Forward the transfer confirmation email to your Shoeboxed address.

- Let our Gmail plugin pick up emailed confirmations on its own.

- Upload or drag and drop on the website.

We keep everything for as long as you have an account, so the deposit slip from three Aprils ago is one search away.

Keep every bank receipt without the shoebox

Getting a bank receipt is easy: the bank hands you one every time. Keeping fifty thermal slips readable and findable years later is the hard part, and that's the job Shoeboxed does. Your deposit slips, your fuel receipts, and your transfer confirmations all land in the same searchable account, each one backed by the original image. And even if you ever leave, you can download everything.

Never lose a receipt again. Join the businesses that scan receipts, sort them into categories, and build IRS-ready expense reports with Shoeboxed. See how it works.

For the bigger system your bank slips fit into, here is our guide to receipt organization and management.

Frequently asked questions about bank transaction receipts

What is a bank receipt?

The record a bank gives you when money moves: a deposit slip, an ATM receipt, a transfer confirmation, or a teller printout. It shows the date, amount, transaction type, the last digits of your account, and a reference number the bank can use to find the transaction again.

Is a bank statement the same as a bank receipt?

No. The receipt covers one transaction and arrives on the spot, and the statement lists the whole month. The IRS accepts a legible statement as proof an electronic payment happened, but it wants the bill or itemized receipt with it to show what the money bought.

How do I create a bank receipt?

The bank creates the receipt when the transaction happens, so you can't make one yourself. What you can prepare ahead is the deposit slip you hand the teller. Our free tool CheckDeposit.io prints a filled-out deposit slip for any US bank. Ask the teller to stamp your copy, and that stamped copy is your receipt.

Do banks still give paper receipts?

Yes, the ATM is required to make one available for transfers over $15, but most records now live in your bank app. Across the 3.5 million receipts our customers sent us since January 2024, fewer than 1 in 100 came from a bank.

Are screenshots of bank transactions good enough for the IRS?

Yes, for proving the payment happened. The image needs to show the amount, who you paid, and the date the payment posted. For a deduction, keep the itemized receipt or bill with it, because proof of payment alone doesn't show what the money bought.

Why do I need a bank receipt?

Two reasons. The reference number lets the bank trace that exact transaction if a deposit goes missing or a transfer never lands. And at tax time, the IRS lists bank deposit slips among the documents that prove your gross receipts, the income side of your return.

Should I shred old bank receipts?

Once you're past the record-keeping window, shred them instead of trashing them, the same as any financial paper. The slip shows only the last digits of your account, so the risk is small, but it still shows your bank, your balance, and your habits. Scan first, then shred without losing the proof.

Final thoughts

A bank transaction receipt is a small thing with one job: proving a specific deposit, withdrawal, or transfer happened. Keep any slip that touches your business, get the image saved before the thermal paper fades, and let the statement handle the monthly overview.

The paper will not take care of itself, and that is the part we handle. Scan the slips, file them, and the records will outlast the ink.

About the author. I'm Doug. I bought Shoeboxed in late 2025 with an SBA loan after fifteen years of running other people's companies as CEO. I'd used Shoeboxed myself back in 2010 at a previous gig and called it magical even then. I use it daily now. Small business owners deserve every dollar they're legally entitled to keep, which is why I bought Shoeboxed and work hard to make it better.

Sources

- IRS, Publication 463, on what counts as adequate proof of an expense, and on canceled checks needing a bill alongside them.

- IRS, Publication 583, on deposit slips proving gross receipts and on when account statements prove payment.

- IRS, How long should I keep records, on the 3, 6, and 7 year windows.

- Cornell Law School LII, 12 CFR § 1005.9, the Regulation E rule requiring receipts at ATMs and electronic terminals.

30 Seconds Could Save You Thousands on Taxes

Self-employed? Get an instant, personalized tax-savings estimate.