What Deductions Can You Claim Without Receipts? (the Cohan Rule)

Lost the receipt? You can still claim the deduction. Here's the IRS-backed way: the Cohan Rule, the $75 rule, bank statements, and an audit-proof log.

Yes, you can still deduct a business expense you paid for but lost the receipt for. The IRS and the courts have allowed it for almost a hundred years, and there's a famous case that proves it.

There's a catch, though, and it trips up a lot of people. Three kinds of expense (travel, business gifts, and your car) need solid records no matter what, and you can't estimate them. Everything else you can still deduct without the receipt, as long as you keep an IRS-compliant expense log: what you spent, when, where, and why. That log is the whole game, and I'll show you how to keep one without the headache.

The short answer: yes, with one big exception

The tax law here is short and plain. You can deduct "all the ordinary and necessary expenses paid or incurred during the taxable year in carrying on any trade or business." It never says "as long as you kept the receipt." So here's how it shakes out in practice:

- For most expenses, the receipt isn 't the hard part. Supplies, software, your website, advertising, subcontractors, fees: nobody's going to demand the original slip. A bank statement plus a note of what it was for will back them up, big or small. You just have to show the expense was real and what it was for.

- Travel, gifts, and your car are stricter. Keep a log no matter what: amount, date, place, and business purpose. For these three, you also need the paper receipt once an expense hits $75 or more, and for any hotel. Under $75, like a lunch on the road, the log alone does it.

That's the whole rule. The receipt is almost never the thing that saves your deduction. The expense log is.

So where does that leave the $75 you keep hearing about? It is not a "claim anything under $75 without a receipt" pass. It only lives inside those strict three (travel, gifts, your car): on those, an expense under $75 skips the paper but still goes in the log. For your everyday expenses, the $75 number isn't even part of the conversation.

Now, the 1930 court case that proves you can deduct with no receipt at all.

Meet the Cohan Rule, the 1930 case that still saves deductions

George M. Cohan was a Broadway showman, the "Yankee Doodle Dandy" guy. He spent a fortune wining and dining people for his shows, and he deducted all of it. The trouble was he kept almost no records, so when the IRS looked at his return and saw no receipts, it threw the deductions out entirely.

Cohan took it to court, and in 1930 the Second Circuit Court of Appeals sided with him. The judges figured a man clearly spends real money entertaining for a business like his, so wiping out every dollar was wrong. Here's the line tax lawyers still quote today:

"Absolute certainty in such matters is usually impossible and is not necessary; the Board should make as close an approximation as it can, bearing heavily if it chooses upon the taxpayer whose inexactitude is of his own making. But to allow nothing at all appears to us inconsistent with saying that something was spent."

That's the whole idea behind what's now called the Cohan Rule. If you plainly incurred a real business expense, a court can let you deduct a reasonable estimate instead of zero, even when the paperwork is gone.

Two things keep it honest. The estimate has to be reasonable, and the judge gets to "bear heavily" against you for being sloppy, which is a polite way of saying they will round down. So treat the Cohan Rule as a safety net, not a plan. You don't want to live there.

Where the Cohan Rule stops: travel, gifts, and your car

For three kinds of expense, the Cohan Rule doesn't apply at all.

Congress decided it was too generous for the costs people abused the most, so it passed a stricter law, Section 274(d). For these three, records are required and a guess won't do:

- Travel away from home, including the lodging and meals you have on the road

- Business gifts , which are capped at $25 per person per year

- Listed property , which for most small businesses means your car

For anything on that list, the IRS wants four facts: the amount, the date, the place, and the business purpose. An estimate won't cut it, and a court can't bail you out with the Cohan Rule the way it did for Cohan himself.

This is also where I have to bust a myth. A lot of people believe there's some magic dollar amount you're allowed to "claim without receipts" in the United States. There isn't. That idea drifts over from other countries' tax rules. Here's how the real lines fall.

| Expense | Claim it without the receipt? | What you need instead |

|---|---|---|

| Supplies, software, equipment | Yes | Bank or card statement plus a note of what it was for |

| Advertising, contractors, fees | Yes | Statement or invoice plus the business purpose |

| Travel, lodging, and meals on the road | No estimating | Always a log (amount, date, place, purpose). Receipt also needed for lodging, or any expense of $75+. Under $75, the log alone is fine. |

| Business gifts | No, capped at $25 | A record of the gift and who received it |

| Your car (listed property) | No estimating | A mileage log of your business trips and miles |

That $75 line matters more than people realize, so it gets its own section next.

What counts as proof when the receipt is gone

Receipt or no receipt, the IRS spells out what it accepts as proof. Its own recordkeeping page lists what backs up a business expense:

"Documents for expenses include the following: Canceled checks or other documents reflecting proof of payment / electronic funds transferred; Account statements; Credit card receipts and statements; Invoices. Note: A combination of supporting documents may be needed to substantiate all elements of the expense."

Read that last note twice, because it's the key. No single piece has to do everything, so you stack them.

A line on your bank statement proves you paid $312. The email confirmation proves who you paid and what you bought. Your calendar proves the meeting happened. Together they tell the whole story even though the cash-register slip is long gone.

So when the receipt is missing, what stands in for it?

- Bank and credit card statements , which prove the amount and the date

- Canceled checks or a record of the transfer

- Invoices, order confirmations, and emails from the seller

- Calendar entries that show the trip or the meeting

- A written note of what the expense was for, made while you still remember

And yes, the IRS accepts a clear photo or scan of a receipt the same as the paper, so a picture on your phone counts.

That last one, the written note, does more work than all the others combined, and it deserves its own section.

The one thing you never skip: keep the log

Here's the $75 rule in full, because it's the one people get wrong. We go deeper in our guide to IRS receipt requirements and the $75 rule, but here's what you need.

It covers the strict three: travel, gifts, and your car. For an expense in that group, the IRS only requires a paper receipt once it hits $75. Lodging is the lone exception and always needs one. So a $40 lunch on the road needs no receipt, but a hotel bill always does.

In real life it shows up mostly on travel. A business gift is capped at $25, so it's always under the line, and your car runs on a mileage log instead of a stack of receipts. Travel and meals on the road are where the $75 line comes into play.

That sounds like a freebie, and in a way it is, but read the fine print. The same rules say you still have to keep "an account book, diary, log, statement of expense, trip sheets, or similar record." So the receipt is optional under $75. The log never is.

That's the whole game. The thing the IRS wants from you in an audit isn't a shoebox of faded slips. It's a clean record showing, for each expense, four facts:

- The amount

- The date

- The place or vendor

- The business purpose

That log can be a spreadsheet, a paper notebook, or a note on your phone, with one line per expense. The format doesn't matter, but keeping it does.

Keep that log, written at or near the time you spent the money, and you've done the part that holds up. Lose the receipt but keep the log, and you're usually fine. Keep every receipt but never build the log, and you've got a pile of paper that still needs hours of sorting before it means anything to an auditor.

What our customers' receipts tell us about real life

I bought Shoeboxed in late 2025, and one of the first things I did was go digging in our own data. Since 2007 we've scanned more than 57 million receipts for over 552,000 small businesses, so it's a good window into how people keep books in real life, as opposed to how the articles say they should.

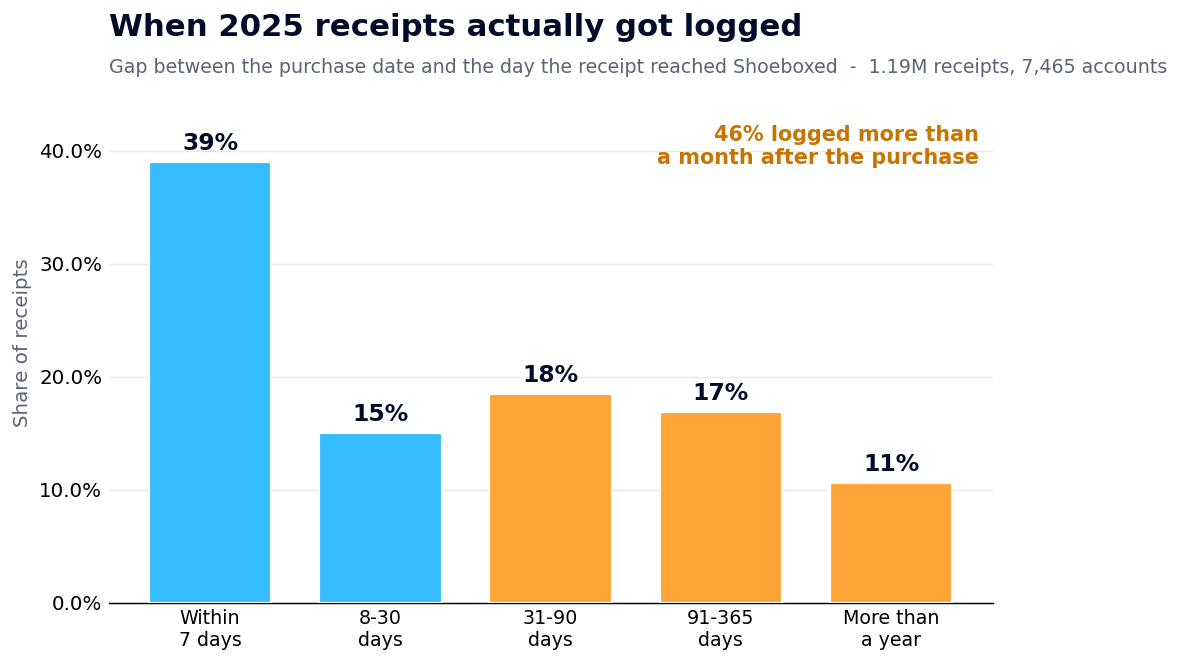

Here's what jumped out. I looked at every receipt our customers logged in 2025, about 1.4 million of them across 7,465 active accounts, and measured the gap between the date on the receipt and the day it reached us.

Of the 2025 receipts where we could compare the purchase date to the logging date, nearly half landed more than a month after the money was spent.

Of the 2025 receipts where we could compare the purchase date to the logging date, nearly half landed more than a month after the money was spent.

Of the receipts where we could compare both dates:

- 46% were logged more than 30 days after the purchase

- 27% showed up more than 90 days later

- About 1 in 9 (11%) arrived more than a year after the money was spent

- On top of that, 37.5% of all 2025 receipts came in with no expense category at all, which is the same as not writing down what the expense was for

I'm not scolding anybody here, because this is how running a business goes. You're out doing the work, not filing paper at the register.

But the numbers tell you something useful. Real bookkeeping almost always happens after the fact, weeks or months later, right when the paper receipt is already in a landfill. So the skill that saves your deductions isn't hoarding receipts. It's rebuilding the expense cleanly once the receipt is gone.

How to reconstruct an expense the IRS will accept

When you're staring at a charge and the receipt is nowhere, here's the order I'd work in.

Rebuilding a missing receipt: the bank statement gives you the amount and date, the email gives you the vendor, and a quick note gives you the business purpose.

Rebuilding a missing receipt: the bank statement gives you the amount and date, the email gives you the vendor, and a quick note gives you the business purpose.

- Start with the statement. Pull up the bank or credit card statement and find the charge. That nails the amount and the date, two of your four facts, right off the bat.

- Find the second document. Search your email for the vendor's name plus the word receipt or invoice, like "Staples receipt." An order confirmation or a "thanks for your purchase" note usually hands you the vendor and what you bought.

- Write down the business purpose now. This is the piece only you can supply, and it fades fast. One plain sentence does it: "Lunch with Maria to talk through the spring contract." Write it today, not next April.

- For the strict ones, log all four facts. If it's travel, a meal, a gift, or your car, make sure your record shows the amount, date, place, and purpose, and hang onto the receipt too if it ran $75 or more. For the car, that means a running mileage log of your business trips.

- Keep it for at least three years. The IRS generally asks you to hold records for three years from when you filed, though some situations call for longer, so when in doubt hang on to them. Store the statement, the email, and your note together so they're easy to find later.

Do that and you've rebuilt a receipt out of evidence the IRS already trusts. It works, but it's a fair amount of digging, every single time.

The easier fix: keep great records without the work

Everything above is your fallback for when the receipt is already gone. The smarter move is to not lose it in the first place. You can deduct without receipts, but keeping them, plus a clean log, is what really protects you if you ever get audited. We built Shoeboxed so that takes almost no effort.

Catching a receipt is dead simple, however it shows up:

- Snap a photo. In the Shoeboxed app, take a picture of anything and it's captured. The app also tracks your drives and creates mileage receipts for you automatically , with the map and the miles, which quietly handles that tricky "listed property" car rule.

- Upload, or drag and drop on the web app.

- Forward it from your inbox. Any receipt that lands in your email, just forward it in.

- Connect your Gmail and we'll watch your inbox for receipts and pull them in for you, no work on your end.

- Mail us the paper. Stuff a month of crumpled receipts in our prepaid Magic Envelope and we scan and organize them for you. It's like having a bookkeeper in your mailbox.

However it arrives, we read each receipt and pull the amount, the vendor, and the date off the page, then file it into a clean, compliant log, the exact fields the IRS wants.

Then we hang on to it. For as long as you're a customer, your receipts, your records, and your log stay put, so if the IRS comes knocking three years down the road, it's all right there. You can export the whole thing any time for taxes, invite your bookkeeper right into your account so they grab what they need without a single email, and if you ever leave us, you can download everything on your way out.

The point is simple: keep amazing records, and let us make it easy. You can start with Shoeboxed whenever you're ready, risk-free with a 30-day money-back guarantee.

One more free tool while you're here. The home office deduction is the write-off people most often skip, usually because they never tracked the costs, which is the same root problem as a missing receipt. Our free home office deduction calculator does the math from your address, no signup required.

Frequently asked questions

Can I claim business expenses without receipts?

Usually, yes. For ordinary business costs like supplies, software, advertising, or contractor payments, you can claim the deduction without the receipt as long as you can show the expense was real and what it was for, using a bank statement, an invoice, or a written record. Travel, business gifts, and your car are the strict exceptions, and those always need a log.

How much can I claim without receipts?

There's no flat dollar amount you're allowed to "claim without receipts" in the U.S., despite a popular myth. What does exist is the $75 rule for travel: you don't need a paper receipt for a travel expense under $75, such as a meal on the road, though lodging always needs one. Even then, you still have to keep a log of the amount, date, place, and business purpose.

Can I use bank statements as receipts for taxes?

A bank or credit card statement is solid proof of the amount and the date, and the IRS lists account statements and credit card statements among its acceptable supporting documents. On its own, a statement doesn't show what you bought or why, so pair it with an invoice, an email, or a note of the business purpose. The IRS expects a combination of documents.

What happens if I get audited without receipts?

You're not automatically sunk. If you can show the expenses were real with statements, invoices, and a log written close to the time, the IRS can allow them, and under the Cohan Rule a court can even accept a reasonable estimate for ordinary expenses. The strict categories (travel, gifts, and your car) are the ones most likely to be denied when you have no records, so those are the ones worth keeping carefully.

Sources

- 26 U.S. Code § 162, ordinary and necessary business expenses: law.cornell.edu/uscode/text/26/162

- Cohan v. Commissioner, 39 F.2d 540 (2d Cir. 1930): law.justia.com

- 26 U.S. Code § 274(d) substantiation and § 274(b) gift limit: law.cornell.edu/uscode/text/26/274

- Treas. Reg. § 1.274-5, the $75 documentary-evidence rule and the log requirement: law.cornell.edu/cfr/text/26/1.274-5

- IRS, What kind of records should I keep: irs.gov

- IRS, How long should I keep records: irs.gov

About the author. I'm Doug. I bought Shoeboxed in late 2025 with an SBA loan after fifteen years of running other people's companies as CEO. I'd used Shoeboxed myself back in 2010 at a previous gig and called it magical even then. I use it daily now. Small business owners deserve every dollar they're legally entitled to keep, which is why I bought Shoeboxed and work hard to make it better.

30 Seconds Could Save You Thousands on Taxes

Self-employed? Get an instant, personalized tax-savings estimate.