Is Per Diem Taxable? The Honest Answer, From a Dad Who Runs a Receipt Company

My son became a wildland firefighter, got handed a government travel card and a $68-a-day per diem, and called me with a tax question. Here's the real answer.

Last fall my college freshman called to tell me he wanted to land a job as a wildland firefighter for the summer. I panicked, stayed up half the night googling safety stats, then took a long walk to settle myself down. Now he's on a wildland firefighter crew in Montana, and we're building a site together to help others become wildland firefighters. As we chatted through how much he could make this summer as a wildland firefighter, he told me that they get $68 per day in per diem while on the road for an assignment. He naturally asked three very important questions about the per diem:

- How much does it add up to over the summer?

- Can I keep the difference if I don't spend all of it?

- Do I have to pay taxes on the per diem?

We pulled the data on the first question, and the answer surprised both of us. A summer "internship" as a wildland firefighter pays far more than most people would guess, and the per diem alone is real money on top of the wages.

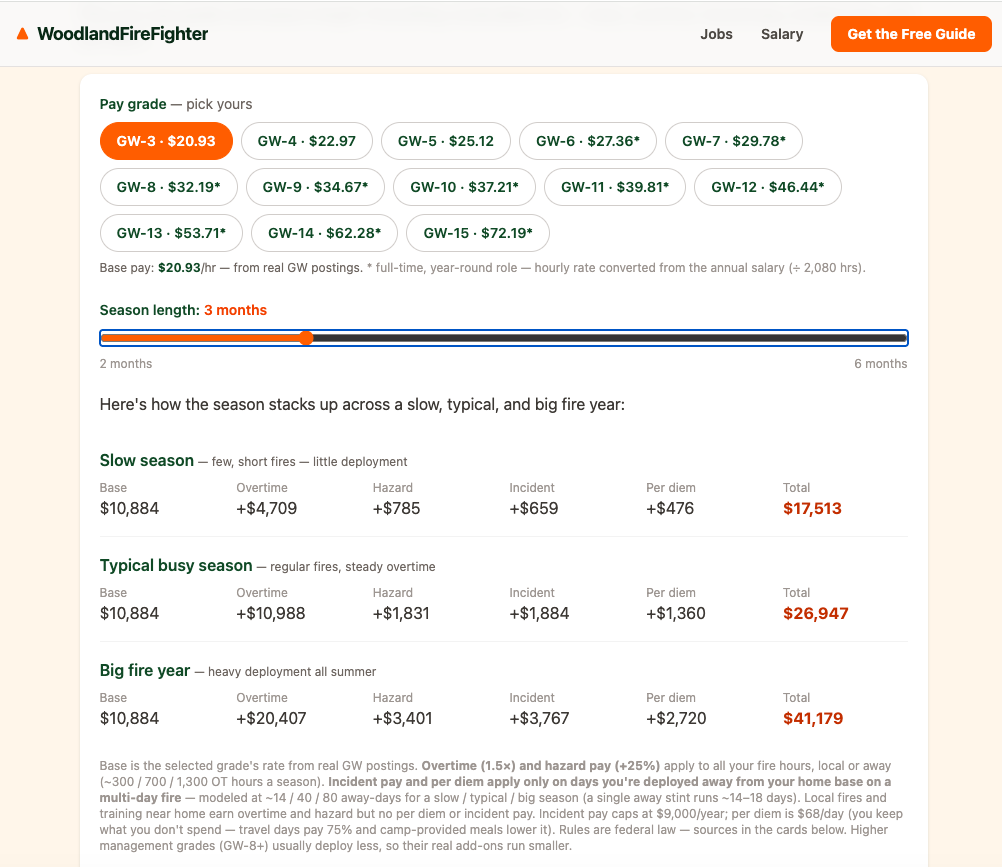

The season calculator on the site we built. Check the per diem column: $476 in a slow three-month season, $1,360 in a typical one, $2,720 in a big fire year. All of it lands on top of wages, and all of it can be tax-free.

The season calculator on the site we built. Check the per diem column: $476 in a slow three-month season, $1,360 in a typical one, $2,720 in a big fire year. All of it lands on top of wages, and all of it can be tax-free.

Quick spoiler on question two: yes, he keeps what he doesn't spend. Question three is the one I turned out to be weirdly qualified to answer. The answer matters for anyone who gets a per diem, not just firefighters.

Is per diem taxable? No, as long as it's paid under an IRS "accountable plan." That means you file an expense report for the trip and keep the receipts the rules require. Per diem at or below the federal government rate isn't taxed. It becomes taxable wages if you don't account for it, or for any amount paid above the federal rate.

That's the short version. The longer version is the part that trips people up, so let me walk through it the way I walked through it with him.

The call: a government card, $68 a day, and a "brutal" form

My son got deployed to his first assignment and came home with a government travel card and a per diem. The card is a GSA SmartPay card. His is what the government calls an Individually Billed Account, a card the GSA says is "issued to an employee designated by the agency/organization in the employee's name." That "in his name" detail is the reason the receipts end up being his problem, not the government's, as you'll see in a minute.

A wildland crew on the line. A standard assignment means 14 days away from home, and the per diem covers the meals.

A wildland crew on the line. A standard assignment means 14 days away from home, and the per diem covers the meals.

The $68 a day he'd mentioned covers his meals on the road. Then came the reimbursement form, which he called, "brutal." He wasn't wrong!

So on top of the money questions, he had two more:

- Do I have to keep all these receipts?

- Why is this reimbursement form so painful?

I run a company that scans receipts for a living, so this was the first time my kid has called me about my day job. I tried not to make it weird.

Quick aside: I'm a huge dork who builds silly little online businesses for fun, so my son and I built one together: WoodlandFireFighter.com. It shows how to land a wildland fire job, open jobs, what the work pays, and the career path available. Honestly? It's a great option for people who love hard work, working outside, and some adventure. No college degree required, it pays well, and comes with great insurance and a pension.

Ok, back to the per diem rule.

The real answer: accountable plan in, taxable wages out

Here's the rule the IRS goes by. It spells it out in its own Per Diem Payments FAQ: per diem payments "are not part of the employee's wages if the payment is equal to or less than the federal per diem rate and the employer receives an expense report from the employee."

Read that twice, because it's the whole game. Two things have to be true for the money to stay tax-free:

- Stay at or below the federal rate. The per diem can't run higher than the federal rate for where you traveled.

- Turn in an expense report. It has to account for the trip: the dates, places, amounts, and business purpose.

Do both and the per diem never shows up as income.

The IRS confirms this on the W-2 side too. In Publication 463, "if your allowance is less than or equal to the federal rate, the allowance won't be included in box 1 of your Form W-2."

That setup, account for it and stay under the rate, is what tax people call an accountable plan. Break either half and you've got a non-accountable plan, and the money flips to taxable wages.

The IRS lists exactly when that flip happens. Per diem becomes taxable when any of these is true:

- No expense report gets filed.

- The report leaves out the date, place, amount, or business purpose.

- A flat amount gets handed out with no report required.

- The payment runs higher than the federal rate.

As the IRS puts it, "if you pay more than the federal per diem rate, the excess will be taxable to the employee."

So my son's $68 a day is tax-free, but only because he's going to do the paperwork.

Where the $68 comes from, and the 75% travel-day rule

The $68 isn't a number his crew made up. It's the federal standard meal and incidental rate. The GSA sets a per diem rate for every part of the country, and for the 2026 fiscal year the standard meals-and-incidentals rate is $68 a day, with standard lodging at $110 a night. Higher-cost cities get higher rates, but most of the country runs on the standard.

Two quirks surprise people. The first travel day and the last travel day only pay three-quarters of the rate. GSA says it plainly: "on the first and last travel day, federal employees are only eligible for 75 percent of the total M&IE rate." The IRS uses the same math, paying "¾ of the standard rate for the first and last day."

The second quirk is the good one, and it answers my son's second question. The meal per diem is a flat allowance, not a refund of your actual meal receipts. If your meals come in under the daily rate, you keep the difference, and it's still tax-free.

Here's what that looks like on my son's first assignment. The standard wildland fire assignment runs 14 days, and his had two travel days on each end, so 18 days total.

| Days | What they are | Meal per diem |

|---|---|---|

| Days 1-2 | Travel days out (75% of $68 each) | $102 |

| Days 3-16 | 14 full days on assignment ($68 each) | $952 |

| Days 17-18 | Travel days home (75% of $68 each) | $102 |

| Total | 18 days | $1,156 |

That's $1,156 in tax-free money for one assignment, as long as the paperwork gets done.

Lodging works differently from meals. There's no flat lodging allowance you get to pocket. You get reimbursed for what you spend on the room, up to the cap, and that's where the receipt rule starts to bite.

The receipt rule that ties it all together

This is the part my son didn't want to hear. Lodging always needs a receipt. Any other expense over $75 needs one too.

That's not his crew being fussy. It's the federal travel rule. GSA, pointing to the Federal Travel Regulation, puts it in one sentence:

"You must provide a receipt to substantiate your claimed travel expenses for lodging and receipts for any authorized expenses incurred costing over $75."

Under that rule, the meal per diem doesn't need a pile of meal receipts, but the hotel and any big single expense do.

The same $75 line shows up in the regular IRS rules for everybody else. Publication 463 says you don't need a receipt when "your expense, other than lodging, is less than $75." Lodging is the permanent exception. Over $75, get the receipt. That one number has been the federal cutoff for decades, and it's a big part of why a receipt company like mine exists. We dug into the whole cutoff in our guide to IRS receipt requirements and the $75 rule.

The stakes: with that card, the receipt is his money

Now back to the card being in his name. This is where I stopped being his dad for a second and started being the guy who runs a receipt company.

The money works like this. His charges go on the card, and the government pays the card off for him. But the government only pays because he files the travel voucher with the required receipts attached. That's the brutal form he complained about. (Some agencies do it the other way around: the worker pays the card, then gets paid back. Either way, the voucher is what makes the money move.)

So picture him losing a hotel receipt, or a $90 gear receipt. The agency can refuse to pay that expense, and since the card has his name on it, he owes the bank for it himself. (If that ever happens to you, here's what to do when you lose a receipt.)

The bigger risk is skipping the voucher. One lost receipt costs him one expense. Skipping the voucher, or filing one missing the dates, places, amounts, and business purpose, costs the whole trip: the per diem stops being an accountable-plan payment, and the IRS can treat all of it as taxable wages.

The receipt isn't paperwork. It's the difference between the government paying his bill tax-free and him eating the cost plus a tax bill.

This is the whole reason I bought Shoeboxed. A firefighter with a government card, a contractor on a job site, a traveling nurse, a small-business owner driving to clients, they're all living the same rule. The per diem is only tax-free if you keep the records. Catching every receipt, especially the ones over $75, is the line between a clean reimbursement and a denied claim.

Your setup probably isn't identical to my son's. Here's how per diem taxes shake out for the most common cases: W-2 employees, 1099 contractors, folks in California, and truck drivers.

Is per diem taxable for W-2 employees?

For most W-2 employees it works exactly like my son's situation. Per diem at or below the federal rate, with an expense report turned in, stays off your W-2 and out of your taxable income. Anything paid above the federal rate is the part that lands in box 1 as wages, and you'll owe tax on that excess.

Want to check your own? A per diem handled right doesn't show up in box 1 of your W-2, the taxable-wages box. The trouble is that box 1 is one blended number, so a per diem that got taxed is buried in there with all your regular pay, and you can't always spot it.

The cleaner move is to ask your payroll or HR person one question: is the travel per diem paid under an accountable plan? If yes, it's tax-free and you're done. If they hand you a flat daily amount and never ask for any expense report, that's the warning sign it may be running through your wages. Get the answer in writing. If it comes back as a no, your employer can often fix it by moving the per diem onto an accountable plan, or you can bring it to whoever does your taxes at filing time.

The catch for employees today: if your per diem does get taxed, you usually can't deduct the unreimbursed difference. The old employee write-off for job travel expenses is gone for most workers. So the accountable plan isn't a nice-to-have, it's the only thing standing between you and a tax bill.

Is per diem taxable for contractors?

If you're a 1099 contractor, you're self-employed, so nobody hands you a tax-free per diem the way an employer does. You deduct your own travel costs on Schedule C instead.

Here's the part most contractors miss. The IRS lets you use the standard meal allowance, about $68 a day in most of the country, for your own business-travel meals. That means you don't have to save every meal receipt. Pub 463 says "you can use the standard meal allowance whether you are an employee or self-employed." Lodging works differently, so you deduct your hotel at actual cost and keep that receipt.

When a client pays you a per diem, the rules technically let them leave it off your income if you give them a full accounting of the trip (our free travel expense report template covers exactly what to track). In practice, though, most contractors just see the per diem land on their 1099 as income. That's fine, because you report it and then deduct your actual travel costs against it on Schedule C, so you're not taxed on money you spent. Keep the hotel folios, the mileage, and any receipt over $75.

And don't sweat the federal-rate ceiling the way a W-2 employee does. If your client pays more than $68 a day, you just report the bigger number and deduct your real costs against it, with no extra penalty for the higher rate.

Two honest catches. You deduct that meal allowance at 50%, the same limit on most business meals, not the full $68. And because this is self-employment income, the per diem also gets hit with self-employment tax, so it's never pure profit in your pocket.

Is per diem taxable in California?

For state income tax, California follows the same federal accountable-plan rule. A proper per diem at or under the federal rate isn't taxable wages on your California return either. But the state adds its own wrinkle for employers, and it's worth knowing if you're the one cutting the checks.

California Labor Code section 2802 says an employer "shall indemnify his or her employee for all necessary expenditures or losses incurred." In plain English, the state expects reimbursements to track real business costs. A flat per diem that ignores actual costs can leave a California employer owing money it didn't properly reimburse. That's a separate issue from the federal tax question, so talk to a California employment attorney before you set a flat daily rate.

Is per diem taxable for truck drivers?

Truckers get their own rules because of the hours they keep. A driver subject to the Department of Transportation's hours-of-service limits can use a special standard meal allowance. For the 2026 federal travel year, the IRS set it at "$80 for any locality of travel in the continental United States" and $86 outside it. That figure resets every October, so check the current number before you file.

Drivers under those DOT limits also get a better deal on meals. Publication 463 lets them "deduct 80% of [their] business-related meal expenses," versus the 50% most everyone else is stuck with. Whether you use the special allowance or actual meal receipts, the substantiation rule doesn't change: keep the log, and keep the receipts the rules call for.

Keep great records, even when the rule lets you skip the receipt

Here's what I told my son, and it's the same thing I'd tell any contractor, nurse, or business owner. Yes, the meal per diem doesn't need a stack of meal receipts. But the smart move is to keep great records anyway, because the moment the IRS questions a number, the records are what save you. The per diem stays tax-free because you can account for the trip, not because you crossed your fingers.

That's the easy part to get right, and it's the thing we built. Snap a photo with the app, forward an email receipt, or mail the paper in, and we scan it, pull out the date, vendor, total, and category, and keep it for as long as you need. When the IRS, or a travel voucher, or an auditor asks two years later, it's all still there. Shoeboxed starts at $9 a month and comes with a 30-day money-back guarantee, so trying it is risk-free.

I'll be honest about why I'm even writing this. My kid is out fighting fires in Montana, calling his dad about expense reports, and building a website with me on the side. Getting to teach him the business and the dull paperwork behind a job that is anything but dull has been an excuse to spend more time together, and that's the part I won't pretend is about taxes.

Frequently asked questions

How much per diem is taxable?

None of it, if it's paid under an accountable plan at or below the federal rate and you turn in an expense report. The taxable part is anything paid above the federal rate, or the whole amount if you never account for it. The IRS treats that excess as wages.

Do you pay taxes on per diem?

Not on a properly accounted-for per diem that's at or under the federal rate. You pay tax only on the excess over the federal rate, or on the whole thing if there's no expense report behind it.

How should per diem be reported on a W-2?

A per diem at or below the federal rate, with an expense report, isn't reported as wages in box 1 at all. Only the excess over the federal rate, or per diem paid with no accounting, gets added to box 1 as taxable wages.

Do I have to keep receipts for per diem?

For the meal portion, no, the flat meal per diem doesn't require meal receipts. But you always need a receipt for lodging and for any single expense over $75. And you always need the expense report showing the date, place, amount, and business purpose of the trip.

About the author. I'm Doug. I bought Shoeboxed in late 2025 with an SBA loan after fifteen years of running other people's companies as CEO. I write about taxes, receipts, and the small-business paperwork nobody warns you about. And yes, I'm the dad in this story, learning the federal travel rules right alongside my son.

Sources

- IRS, Per Diem Payments Frequently Asked Questions

- IRS, Publication 463, Travel, Gift, and Car Expenses

- GSA, Per Diem Rates and Per Diem Frequently Asked Questions, which cite the Federal Travel Regulation receipt rule

- GSA, Travel Charge Card (SmartPay)

- IRS, Notice 2025-54, 2025-2026 Special Per Diem Rates (transportation-industry meal rate)

- California Legislature, Labor Code Section 2802

30 Seconds Could Save You Thousands on Taxes

Self-employed? Get an instant, personalized tax-savings estimate.