How to Write a Check in 2026 (And Why I'm Still Teaching My Kids to Do It)

A step-by-step guide to writing a paper check, written after my 14-year-old asked what a checkbook was. Plus who still uses checks, and why you probably will too.

Last updated: April 2026

My 14-year-old daughter asked me what a checkbook was last week. I laughed. Then I actually thought about it and asked myself, "do people still deposit checks?" Man, did the data shock me when I looked at it.

Turns out Americans still write 11 billion paper checks a year. That's $27 trillion in value , more than every US credit card transaction combined. Might be a good idea to teach your kids how to write one.

TL;DR, the six steps:

- Write today's date, top right

- Name the payee on the "Pay to the order of" line

- Write the amount in numbers in the little box

- Write the same amount in words on the long line (this is where people mess up)

- Memo (optional)

- Sign it, bottom right

Should You (or Your Kid) Actually Learn This?

I asked myself the same question after the kitchen moment. Here's the short answer: yes.

Checks show up in the corners of adult life you can't fully predict. Landlords who won't take Zelle. Contractors who want a physical down payment. Checks from insurance companies after a storm. Tax settlements. Wedding gifts from grandparents. Tithes at church. Invoices from staffing agencies and truckers and small law firms.

In fact: I spent some time digging into 81,000 deposit slips on a free tool I built years ago and matched them against the Federal Reserve Payments Study. The short version: checks aren 't dying, they're specializing. Small business owners, churches, contractors, medical practices, nonprofits, landlords, and anyone with an insurance claim still run on paper. I wrote the full data dive over here if you want the numbers.

So: yes. A little friction in your kid's life now saves an awkward phone call at some point in their twenties. Let's do it.

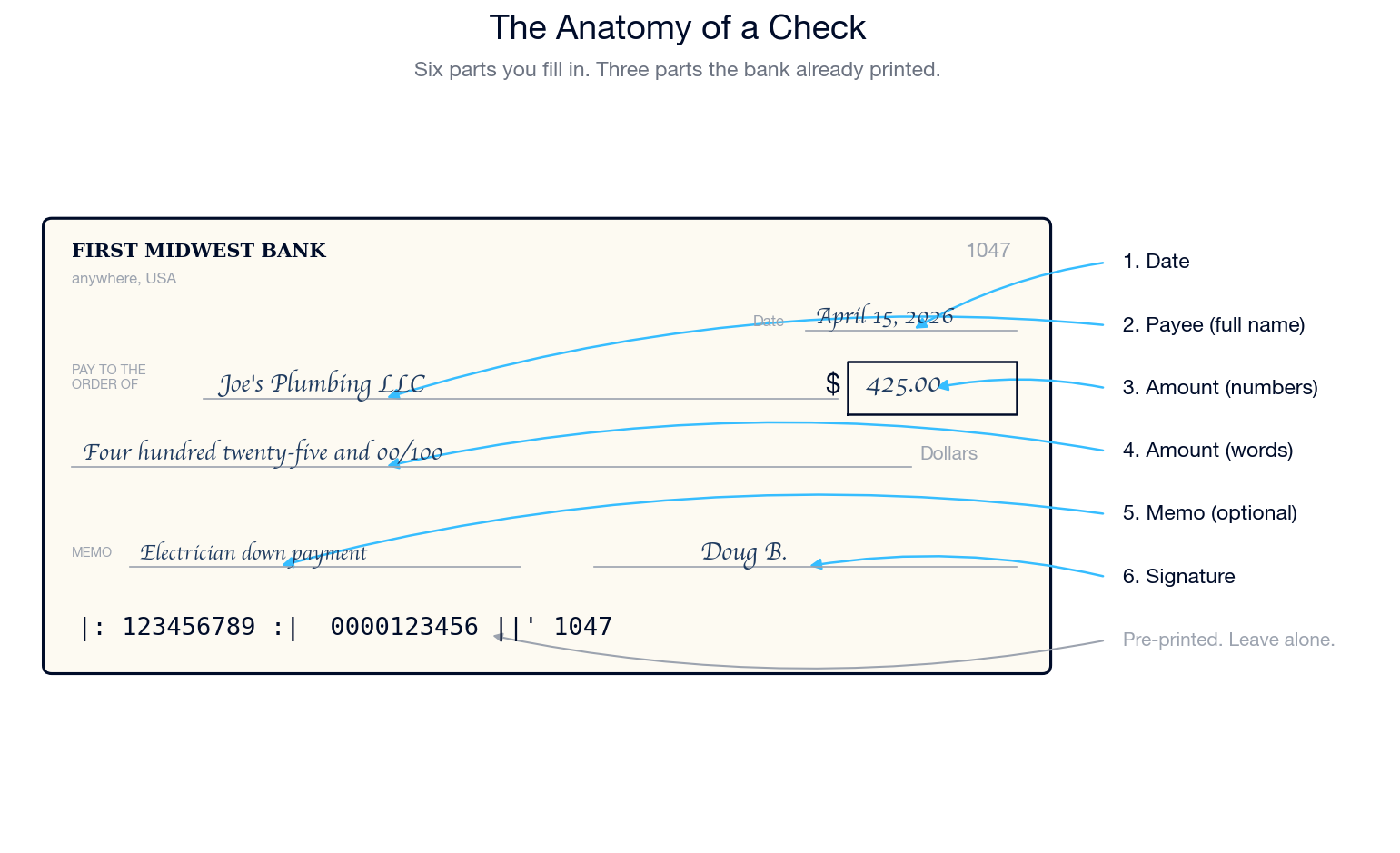

The Anatomy of a Check

Here's what a check looks like, with every part labeled.

Six parts you fill in:

- Date : upper right

- Pay to the order of : the name of whoever gets the money

- Amount (numeric) : the dollar box on the right

- Amount (written) : the long line under the payee

- Memo : optional note for what the check is for

- Signature : bottom right

Three things the bank already printed: the routing number, the account number, and the check number. Your kid doesn't need to care about those. The bank put them there. Leave them alone.

Step by Step: Writing Your First Check

Here are the six steps, with the stuff I wish someone had told me the first time.

1. Write the date

Top right corner, on the "Date" line. Just today's date. Any format works, though MM/DD/YYYY is the most universal.

Here 's the deal: checks typically stay valid for six months from the date you write. So don't backdate anything you don't want someone waiting to cash.

What about post-dating? (Writing a future date.) Technically yes, you can do it. But the law doesn't require banks to honor the date. If someone deposits a post-dated check early, their bank may process it anyway. Don't rely on post-dating to delay a payment.

2. Write the payee

On the "Pay to the order of" line, write the full name of the person or business you're paying. Full legal name. No nicknames. No abbreviations.

If you misspell the payee's name, or leave it unclear, the bank may refuse to cash it. "Joe's Plumbing" is fine, if that is their actual business name. "Joe" is not.

3. Write the amount in the little box

The little box to the right of the payee line, the one with the dollar sign. Write the exact amount in numbers. Example: 425.00 (or 425.50 if there are cents).

Pro tip: start your writing right up against the dollar sign. A gap invites a bad actor to add a digit. Fraud is old, but paper-check fraud is still doing just fine in 2026.

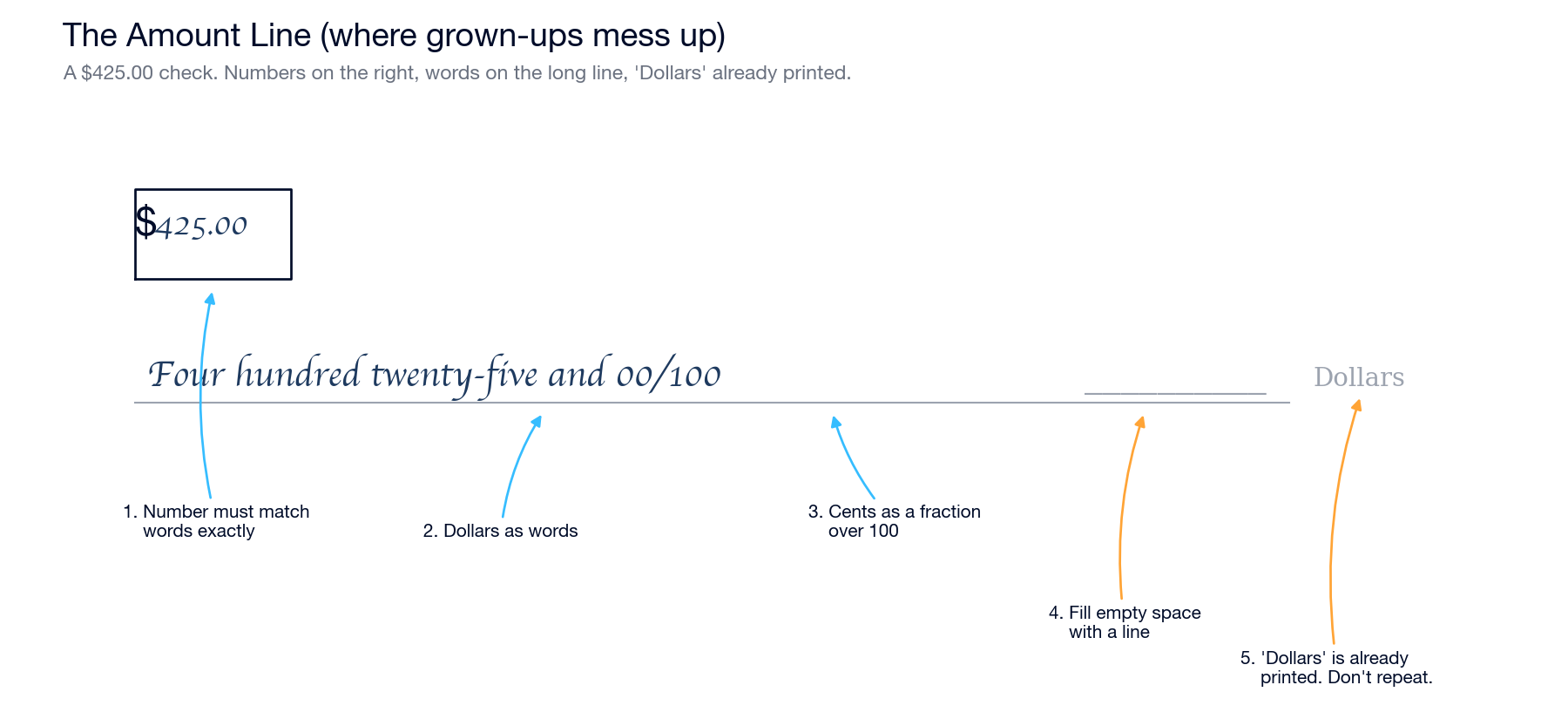

4. Write the amount in words (this is where grown-ups mess up)

This is the long line underneath the payee line. You write the amount out in words. This one step trips up more adults than the other five combined.

The format: dollars as words, cents as a fraction over 100.

- $425.00 becomes: Four hundred twenty-five and 00/100

- $42.50 becomes: Forty-two and 50/100

- $1,200.75 becomes: One thousand two hundred and 75/100

Three things to remember:

- " Dollars" is already printed on the check at the end of the line. Don't write it yourself, or you'll have "Dollars" appearing twice.

- The "and 00/100" piece matters even when the amount is a round number. It tells the bank there are zero cents. Without it, in theory, someone could add cents.

- Draw a line from the end of your writing to where "Dollars" is already printed. That line fills the empty space so nobody can add words.

Now: if the number you wrote in the little box and the amount you wrote in words disagree, the written line legally wins. Banks might catch it. They might not. Get them to agree before you tear the check off.

5. Memo (optional, but useful)

Lower left, on the "Memo" or "For" line. Write what the check is for. "Rent, April 2026." "Electrician deposit." "Son's baseball fees."

This line is for you and your record-keeping, not the bank. The bank doesn't read it.

Pro tip: if you're writing to a business, a specific memo ("Invoice #1047") can help them credit your account faster. Not required.

6. Sign it

Bottom right, on the signature line. Sign it exactly the way your signature appears on file with the bank. For most adults, this is whatever weird scribble you settled on in your twenties and have been doing ever since.

An unsigned check is not a check. It is a piece of paper. I have forgotten to sign a check more times than I would like to admit.

Special Cases

A few things that come up once you start writing checks regularly.

Even dollar amounts. Write "and 00/100" even when the cents are zero. $500.00 is Five hundred and 00/100. Skipping it invites fraud.

Big amounts. For $5,000 or more, pay attention to commas in the numeric box ($5,000.00, not $500.00). For the written line, just write it out: Five thousand and 00/100. No commas needed in the words.

Cents only, no dollars. Writing a check for 75 cents (you wouldn't, but just in case) looks like: $0.75 in the box, Zero dollars and 75/100 on the line. Rare in the wild.

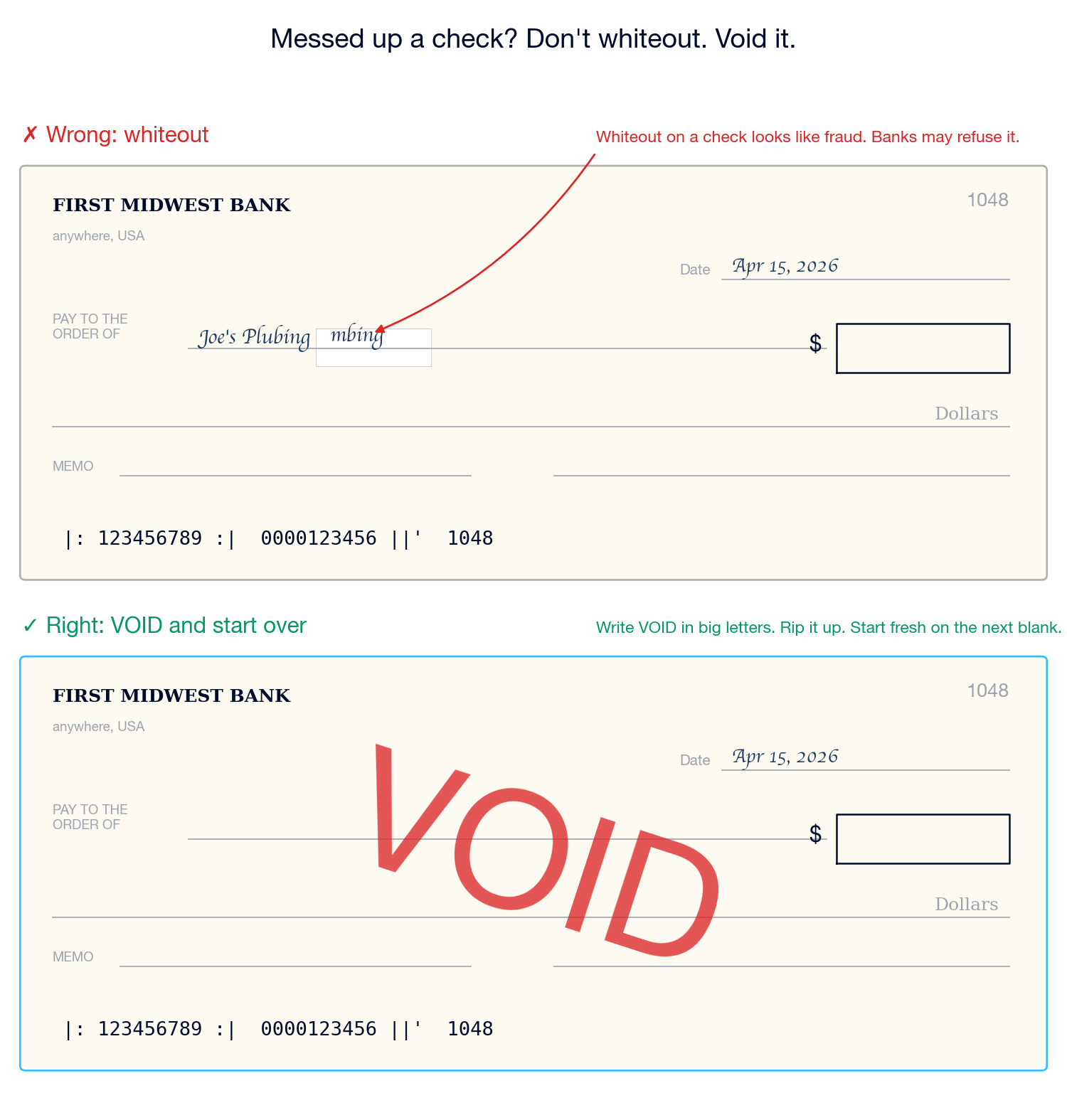

Making a mistake. If you write something wrong, do not use whiteout. Banks may refuse a whited-out check because it looks like fraud. The right move: write VOID in big letters across the front, rip it up, and start fresh on the next blank. Some people keep the voided check for their records.

Writing a check to yourself. Totally legal. On the "Pay to the order of" line, write your own full name. Sign it, endorse the back, and deposit it at a different account. People do this to move money between their own accounts when they don't feel like logging into online banking.

" Pay to cash." Technically legal. Also a terrible idea. Anyone who finds a "pay to cash" check can cash it. Don 't do this. Ever.

Five Mistakes Adults Still Make

After doing this for thirty years, I still mess one of these up every couple of years.

1. The numeric and written amounts don 't match. Legally, the written line wins. Practically, banks may return the check. Always re-read both fields before tearing the check off.

2. Forgetting to sign. An unsigned check is not a check. The recipient's bank will return it. You'll find out three weeks later, usually at the worst possible moment.

3. Writing in pencil or non-permanent ink. Banks want blue or black ink, permanent. You can erase pencil. Gel pens smudge. Keep a basic pen in the checkbook.

4. Not recording it. Somewhere in the back of the checkbook there's a little register. Record the check number, date, payee, and amount. Modern online banking catches everything after the fact. But if you write the check on Friday and the recipient deposits it three weeks later, your account balance thought you had the money the whole time.

5. Running out of deposit slips before checks. This one trips up small business owners specifically. Your bank gives you a checkbook with deposit slips in the back. You use the checks, but the deposit slips sit there. When the slips run out and you still have checks left, your bank wants to sell you a new book.

Quick plug and then I 'll move on: I got so annoyed at this that I built a free website called CheckDeposit.io back in 2019 that prints a deposit slip for any US bank. No signup, no ads. Your kid is welcome to use it.

What Happens After You Write It

The recipient takes the check to their bank and deposits it. Physically, in person, or by snapping a photo with their phone (mobile deposit).

From there, most checks clear in 1-3 business days. Your account shows the money leaving. Their account shows it arriving. Done.

If the check bounces (you didn't have enough money in the account), your bank charges you a fee, their bank charges them a fee, and the transaction reverses. That's a memorable thing to explain to a teenager. Save it for the right moment.

For most people, most of the time, you write the check, hand it over, forget about it, and two weeks later you notice it cleared.

Who Still Writes Checks in 2026?

A short list, from what I saw digging through that deposit-slip data:

- Small businesses (staffing agencies, trucking companies, contractors, independent consultants)

- Medical and dental practices (insurance reimbursements and copays)

- Churches and nonprofits (tithes, donations, fundraising)

- Landlords (a stubborn minority who still want rent by check)

- Insurance companies (claim payouts)

- Law firms (retainers, settlements)

- Grandparents (a universal constant)

- The federal government, until recently. Per IRS.gov on Executive Order 14247, paper IRS refund checks phased out September 2025. That still left about 7% of 2025 refunds mailed before the switch.

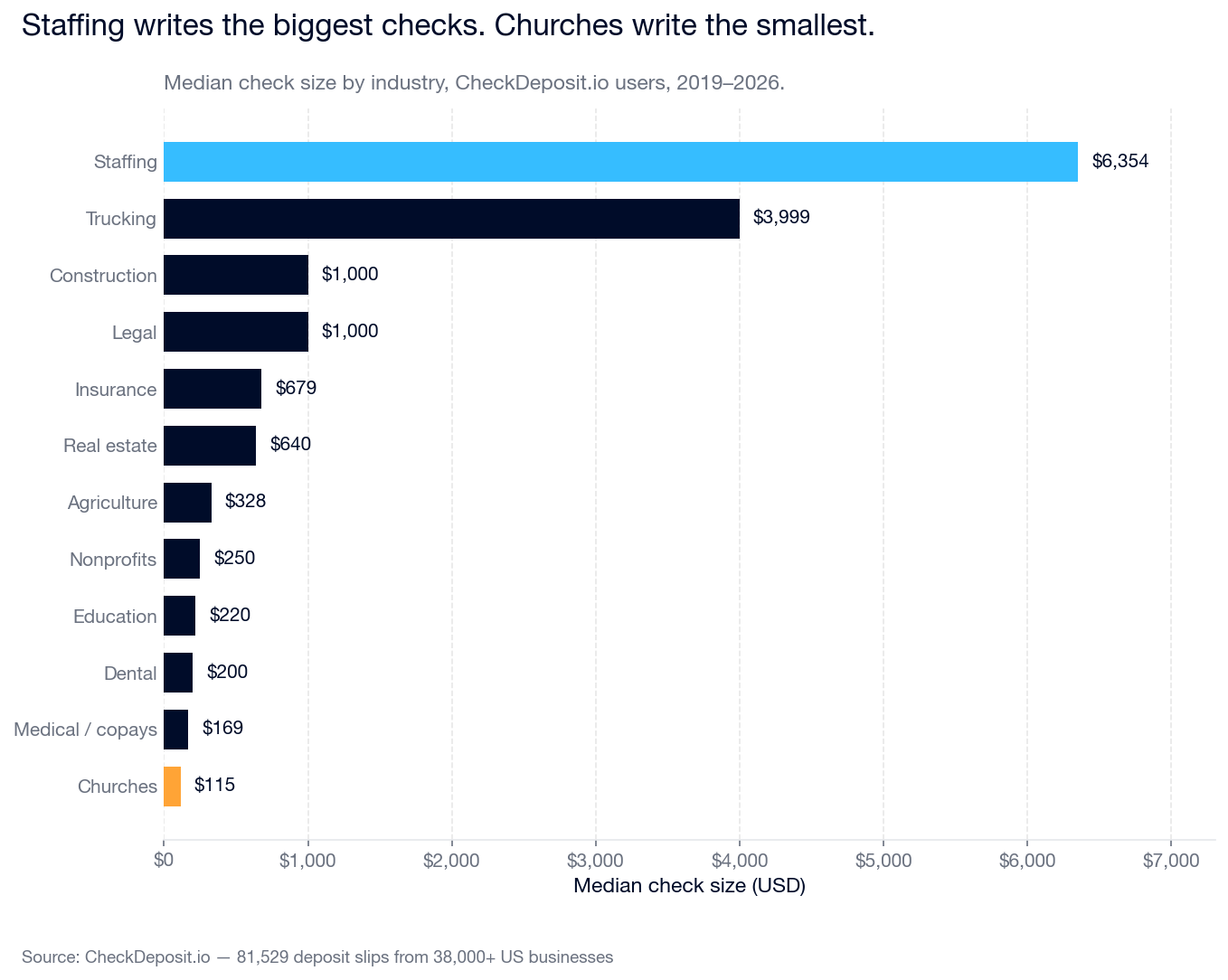

The most surprising thing I saw in the data: the industries with the biggest checks aren't the ones you'd guess.

Staffing agencies write the biggest median check ($6,354). Churches write the smallest ($115, because that is what tithes actually look like). The AFP's annual payments survey has shown for years that 30-40% of B2B payments are still made by check. The industries above are that 30-40%.

If your kid ever rents an apartment, starts a side hustle, gets paid by an insurance company, tithes at church, or hires a plumber, they will touch a check. Probably sooner than you expect.

Frequently Asked Questions

How do I write a check with cents?

Dollars as words, cents as a fraction over 100. $42.50 is Forty-two and 50/100. Always include the cents fraction, even for round numbers (and 00/100) so nobody can add cents later.

How do I write a check for thousands of dollars?

For the numeric box, include the comma: $5,000.00 or $12,500.00. For the written line, no commas needed. Just the words: Five thousand and 00/100 or Twelve thousand five hundred and 00/100.

Do I write "and" in the dollar amount?

The "and" goes between the dollars and the cents fraction. Not between "hundred" and the next word. It's: "Four hundred twenty-five and 00/100." Not "Four hundred and twenty-five." That's the grammatical rule. Most banks don't care, but it is technically the right way.

How long is a check good for?

Usually six months from the date written. After that, banks may refuse to cash it. The technical term is "stale-dated." If you find an old check, contact the person who wrote it and ask for a fresh one. Don't try to cash it anyway.

Can I write a check on regular paper?

Technically, yes. A check just needs the right information: your name, the bank's name, routing and account numbers, the date, the amount, and your signature. In practice , pretty much every bank will refuse a handwritten "check" on notebook paper in 2026, because of fraud controls. Use a real check.

What do I do if I make a mistake on a check?

Write VOID in large letters across the front, rip it up, and start on the next blank check. Don't whiteout. Don't cross out and initial. Just start over.

What if the person I 'm writing the check to doesn't want to deposit it?

That's their problem. Once you hand over a signed check, the money is earmarked for them. You can usually cancel it by calling your bank and requesting a "stop payment," which costs a fee (usually $20-$35). Only do this if you have a real reason.

Can I write a check to myself?

Yes. Write your full legal name on the "Pay to the order of" line, sign it, endorse the back with the same signature, and deposit it. People do this to move money between banks. In 2026, a wire transfer or ACH is usually faster and free. But a check still works.

Quick update on the 14-year-old: I walked her through a practice check that weekend. She got it in about five minutes. Then she asked why grown-ups still keep a whole notebook for this when we could just tap a phone. I am still working on that answer. If any of my kids are reading this in fifteen years, I promise: your dad had a good reason. I just can't remember it right now.

Own a Small Business? Shoeboxed Can Help.

If you own a small business and you're still writing checks (a lot of you are, per the data), the IRS also wants you to keep the receipts for whatever you wrote the check for. That part I can help with. I run a company called Shoeboxed that scans and organizes those receipts for you. Real humans in North Carolina do the scanning. There's a risk-free trial if you want to try it.

Need to Deposit a Check, Not Write One?

If you run a small business and checks come to you too, Shoeboxed has a free tool for that side of it called CheckDeposit.io. It prints a deposit slip for any US bank in about 30 seconds. No signup, no ads. Use it as many times as you want.

Doug

30 Seconds Could Save You Thousands on Taxes

Self-employed? Get an instant, personalized tax-savings estimate.